Latest Home Loan Interest Rates 2026 by top banks and HFCs are mentioned in the table below:

| Name of Lender | Interest Rates# |

|---|---|

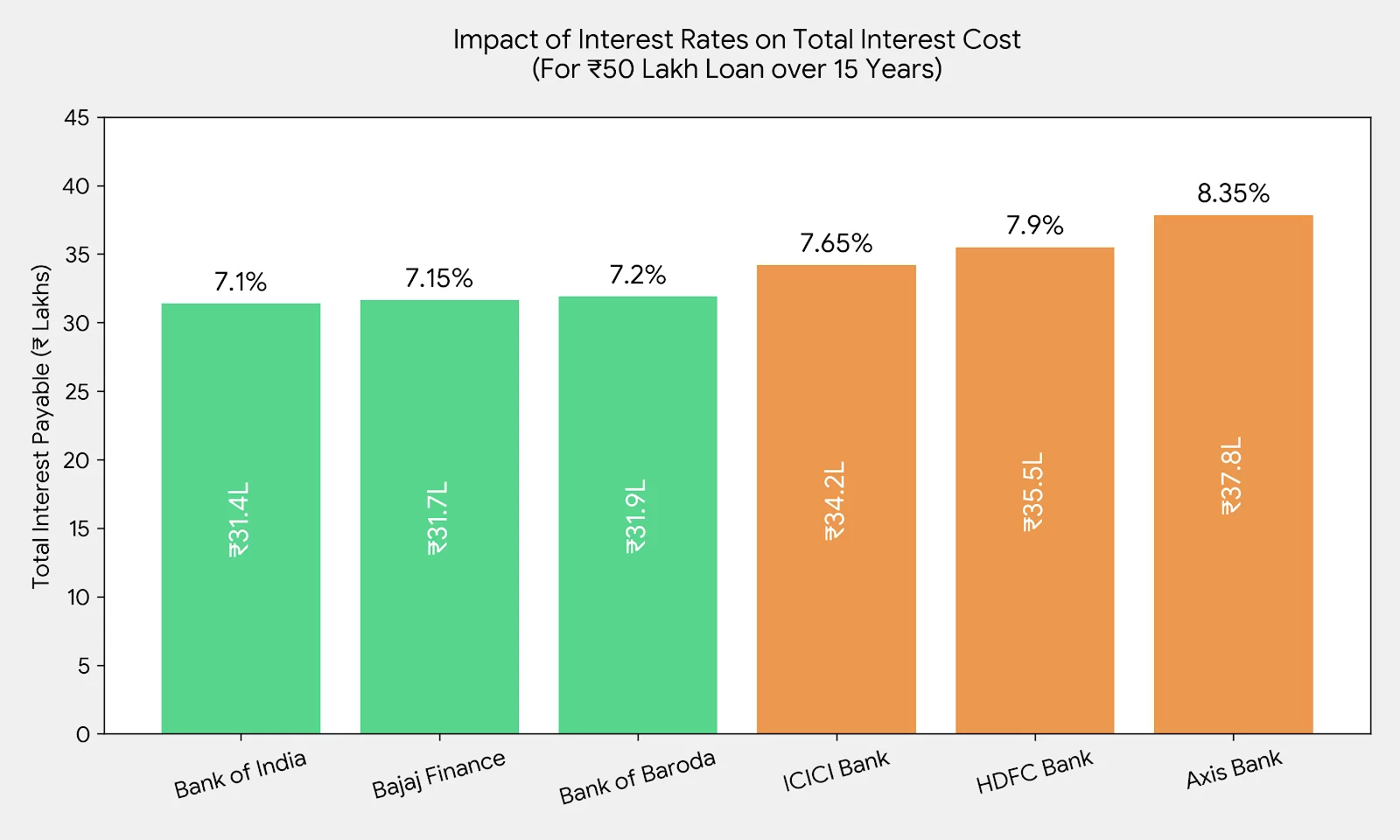

| Axis Bank | 8.00% - 11.90% p.a. |

| Bajaj Housing Finance | 7.25% p.a. onwards |

| Bank of India | 7.10% - 10.25% p.a. |

| Canara Bank | 7.15% - 10.00% p.a. |

| Easy Home Finance | 8.99% p.a. onwards |

| Federal Bank | 7.30% - 10.75% p.a. |

| Godrej Housing Finance | 7.65% p.a. onwards |

| HDFC Bank | 7.20%* p.a. onwards |

| HDFC Sales Pvt. Ltd. | 7.20%* p.a. onwards |

| Home First Finance | 8.00% p.a. onwards |

| ICICI Bank | 7.50% p.a. onwards |

| IDBI Bank | 7.35% p.a. onwards |

| IDFC FIRST Bank | 8.85% p.a. onwards |

| India Shelter Home Loan | 10.50% p.a. onwards |

| Jio Housing Finance | 8.20% p.a. onwards |

| L&T Finance Limited | 7.65%* p.a. onwards |

| LIC Housing Finance Limited | 7.15% - 10.00% |

| Piramal Capital Housing Finance | 9.99% p.a. onwards |

| PNB Housing Finance | 7.50% p.a. onwards |

| Punjab & Sind Bank | 7.30% - 10.70% p.a. |

| Punjab National Bank | 7.20% - 9.30% p.a. |

| RBL Bank | 8.20% p.a. onwards |

| Sammaan Capital (Formerly known as Indiabulls Housing Finance) | 8.75% p.a. onwards |

| Shubham Housing Finance | 10.45% p.a. onwards |

| State Bank of India | 7.25% - 9.05% p.a. |

| Tata Capital Housing Finance | 7.75%* p.a. onwards |

*when applied through Paisabazaar Home Loan Interest Rates as of 3rd June 2026