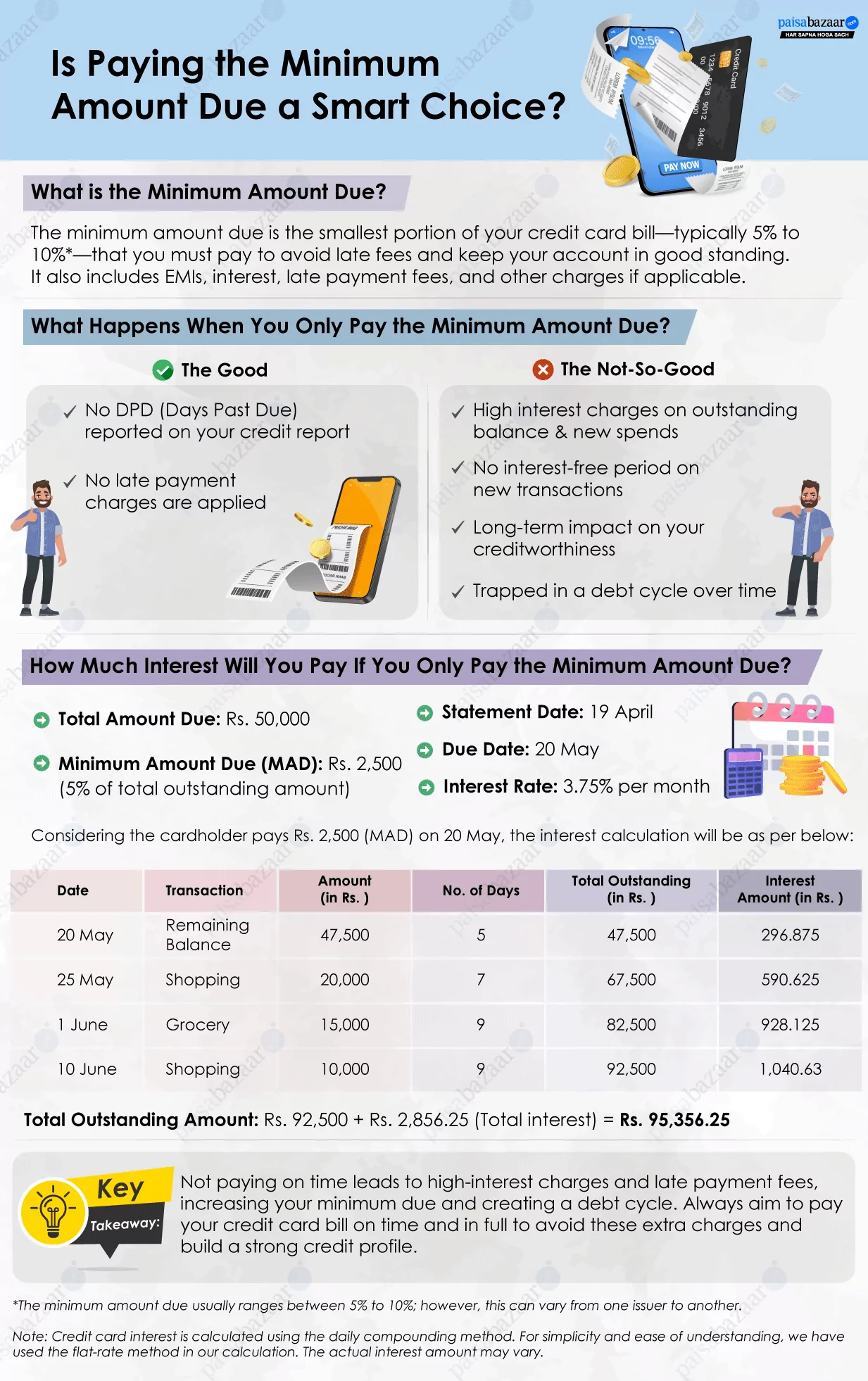

The minimum amount due is the smallest portion of your total outstanding credit card bill that must be paid by the due date to keep your account in good standing and avoid late payment charges. Usually, the minimum due ranges from 5% to 10% of the total outstanding amount, though this percentage may vary from one issuer to another.

One important thing to note is that the minimum amount due includes EMIs, interest, fees, and other charges. So, if you have an ongoing EMI, it will also be added to the monthly minimum amount due.