One of the most important factors a CIBIL score depends on is the repayment history. Lenders analyse this section critically at the time of credit approval. They go through every credit product to check for a non-zero DPD in the credit report. Let us understand what a DPD is and how it can impact the credit score.

Days Past Due (DPD) in CIBIL Report

Why Check Credit Score on Paisabazaar ?

Check Credit Score from All 4 Bureaus

Track Credit Score Seamlessly Every Month

Read Credit Report in Multiple Languages

4.5/5

15.6L Reviews

6Cr+Satisfied Customers

4Bureau Coverage

800+Cities across India

Check CIBIL Score & Report worth₹1,200Absolutely FREE Chance to get Accidental Cover up to ₹1Lakh & more

Let’s Get Started

4.5/5

15.6L Reviews

6Cr+Satisfied Customers

4Bureau Coverage

800+Cities across India

Why Check Credit Score on Paisabazaar ?

Check Credit Score from All 4 Bureaus

Track Credit Score Seamlessly Every Month

Read Credit Report in Multiple Languages

How DPD Affects Your Credit Score?

Know All About Days Past Due (DPD) in Your CIBIL Report

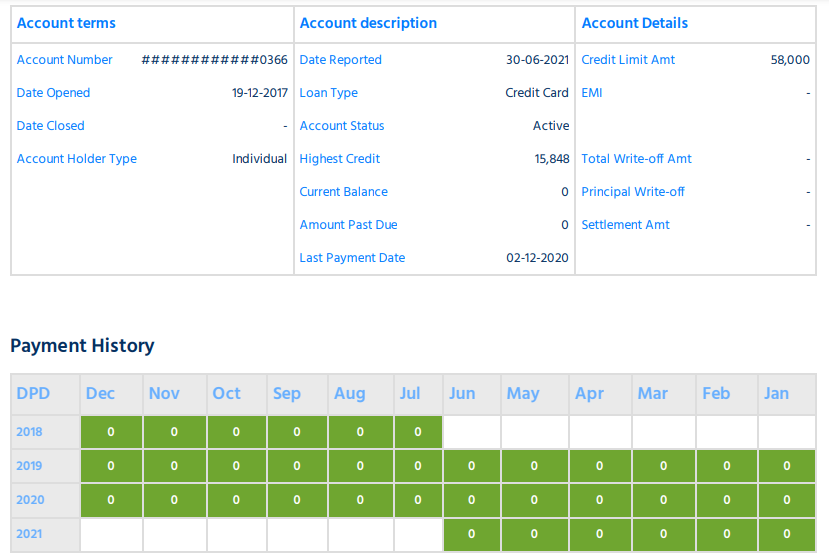

Days Past Due (DPD) indicates the number of days by which a borrower has missed an EMI or credit card payment. DPD is present in the 'Payment History' section of your CIBIL report.

The DPD in the CIBIL report is considered one of the determining factors for lenders while approving or rejecting your loan or credit card application.

Understanding the DPD Calculation Method

If you have made timely payments in the past, your DPD (Payment made within 90 days) will be mentioned as ‘000’. In case you have missed your payment by 40 days, your report will show '40' against the previous month.

There may be instances where "XXX" is mentioned in the DPD in CIBIL. It means that the lender has not provided the payment history details to the credit bureau. You should not worry, if you find it in your credit report, as it has no negative impact on your credit score or your chances of loan or card approval in the future.

Significance of DPD Value

DPD shows how disciplined you have been in making EMI payments in the past. It contains your payment timeline for the past 36 months. While assessing your credit application, the lender checks whether you have missed any payments in the past. If your DPD is '000' for all 36 months, it shows that you have prudently paid off all your credit dues on time and pose a lesser risk to the lender.

Occasionally missing the payment deadline also hurts your credit score and creditworthiness but few lenders might approve your credit application. However, frequent misses and non-payment of dues for long pose a higher risk for lenders and they may refrain from approving your loan or credit card applications.

DPD Updation Frequency in your CIBIL Report

Every time a lender submits your credit data to the credit bureau, it updates the details in your CIBIL report and evaluates and generates your CIBIL score. Your credit score may not change every month, even if the details are provided regularly by the lender.

In case you miss a deadline by 30 days, the Credit Information Company (CIC) or Credit Bureau updates your DPD for that month as '30' in your credit report. Assuming you don’t make the payment and the lender reports it to the bureau the next month again, your DPD would be updated as '60'.

As per the financial experts, it is recommended not to miss the payments by more than 3 months, as it can have a serious impact on your credit score, as well as your creditworthiness may get hampered.

Suggested Read : What is a CIBIL Score

Ways to Report Disputes Regarding DPD Errors

In case you find that your credit report has DPD errors, wherein you made the payment on time for a specific month but your DPD shows a value other than "000" (it means that the lender has reported that you missed the payment by the number of days mentioned in the DPD), you can report this error to the credit bureau.

CIBIL will request verification with the concerned lender and add an "Under Dispute" tag to your credit account. Once the lender sends the correct data to the bureau, it updates the credit report and removes the "Under Dispute" tag.

TransUnion CIBIL also shares an updated credit report containing your refreshed credit score.

Also Read: How to Raise CIBIL Dispute?

Know How to Read/Locate DPD in your CIBIL Report

DPD is mentioned against each of your credit products in the “Payment History” section of the CIBIL report. For example, if you have 3 active credit products, such as SBI credit card, ICICI home loan, and HDFC personal loan, DPD for the past 36 months will be mentioned against each of the credit products separately.

Important Elements of DPD Value

Below states are the abbreviated asset classifications under DPD for availed loans or credit cards:

Common Abbreviations:

It is recommended that you check your CIBIL report regularly for any minor or major errors and get it rectified at the earliest so that your CIBIL score does not fall. Here, you can check free credit reports from multiple credit bureaus and receive monthly updates with no impact on your credit score. It can further help you in keeping track of your DPD and other errors in your credit report, if any.

Other Credit Score Related Articles:

How to Check CIBIL Score for Free with Paisabazaar?

Step 1: Enter your mobile number

Step 2: Verify your number using the OTP

Step 3: Enter your PAN and basic details

Step 4: View your free credit score and get detailed credit report

How to Check CIBIL Score for Free with Paisabazaar?

Step 1: Enter your mobile number

Step 2: Verify your number using the OTP

Step 3: Enter your PAN and basic details

Step 4: View your free credit score and get detailed credit report

FAQs

What does it mean to have DPD in my CIBIL report?

Days Past Due (DPD) is a key indicator in your CIBIL report that signifies the period or number of days a loan EMI or credit card due date has been missed or delayed for any reason. It highlights the defaults or delays in the credit payments of a borrower.

What is the DPD full form in the CIBIL report?

DPD in your CIBIL report stands for Days Past Due, which indicates the number of days by which you have delayed or missed payments of your past or existing loan or credit card, if any.

How do I check DPD in the CIBIL report?

DPD in your CIBIL report can be checked under the ‘Payment History’ section of your CIBIL report. It is considered one of the most vital components of your CIBIL report that indicates your creditworthiness and repayment capacity.

What companies include a DPD in their credit report?

All the Credit Information Companies (CICs) or credit bureaus named TransUnion CIBIL, Experian, Equifax, and CRIF High Mark mention the DPD value. The DPD value is generated by the consumer credit information provided by the banks to the credit bureaus every month.

Where in the CIBIL report is the DPD value listed?

Your DPD value is listed under the 'Payment History' section of your CIBIL report. It is good not to have any numeric against your DPD in your CIBIL report, as it signifies no delayed or missed payment by your side.

What can a borrower do to prevent a negative DPD value?

A borrower needs to pay all his/her credit payments, such as loan EMIs, credit card dues or any borrowed credit payments in time to avoid any negative value against your DPD section in the CIBIL report.

What is considered as 30 Days Past Due?

If you have missed a payment by 30 days, then a DPD will reflect in your credit report, as the credit bureau updates it as '30' for a particular month. However, if you have missed your payments by 2 consecutive months, it shall reflect as '60'.

Can we remove DPD from CIBIL?

As we can not change or edit any details in our credit report, the same way we can not remove or edit DPD from our credit report. As it is an integral and related component of the credit report, it cannot be altered or removed. However, we can wait until the DPD section shows some stability or improvement within a few months of regular and timely payments.

What is the DPD rule in CIBIL?

There is no such DPD rule as stated in CIBIL or any credit report. DPD indicates the number of days the borrower has missed or delayed the payments. So, the higher the DPD is, the lower your creditworthiness and vice versa. Try to pay off all loan EMIs and credit card dues in time to avoid any DPD number in your credit report.

How many Days Past Due are there in the CIBIL report?

The CIBIL report holds DPD information of a maximum of 90 days which is divided into 3 months, wherein the value reflected is 30, 60, and 90 days. These values indicate the number of days that passed or were missed after the payment due date of the loan EMI or credit card bill.

Credit Score Articles

Delayed Credit Score Correction? RBI’s Compensation Framework Explained

Sumit Kumar12 Jun 2026

Does the Length of Your Credit History Affect Your Credit Score

Vandana Punj27 May 2026

I Have 4 Credit Cards and 2 Loans: How to Maximize My Credit Score?

Lepakshi Phogat26 May 2026

How to Manage Multiple Loans Without Hurting Your Credit Score

Neha Singh18 May 2026

How Can Students Build Their Credit Scores Without Income Proof?

Bharti18 May 2026

How Self-Employed Can Build Credit Score

Rupanshi Thapa12 May 2026

How Credit Utilization Ratio Works and What Percentage Should I Maintain

Sushmita Mishra12 May 2026

Why Did My CIBIL Score Drop Without any Reason?

Arvind Kumar08 May 2026

Why Minimum Due Payments Hurt Your Credit Score

Shruti Sharma06 May 2026

Not All Accounts Count: What Impacts Your Credit Score—and What Doesn’t

Samridhi Srivastava05 May 2026

Paisabazaar is a loan aggregator and is authorized to provide services on behalf of its partners

*Applicable for selected customers

Check Credit Score for FREE