Discover practical tips to increase your CIBIL score & Credit Score from 600 to 800 fast, fix common credit mistakes, and build a stronger financial profile for best loan & credit cards offers.

How to Improve CIBIL Score Fast

Why Check Credit Score on Paisabazaar ?

Check Credit Score from All 4 Bureaus

Track Credit Score Seamlessly Every Month

Read Credit Report in Multiple Languages

4.5/5

15.6L Reviews

5.7Cr+Satisfied Customers

4Bureau Coverage

800+Cities across India

Check CIBIL Score & Report worth₹1,200Absolutely FREE Chance to get Accidental Cover up to ₹1Lakh & more

Let’s Get Started

4.5/5

15.6L Reviews

5.7Cr+Satisfied Customers

4Bureau Coverage

800+Cities across India

Why Check Credit Score on Paisabazaar ?

Check Credit Score from All 4 Bureaus

Track Credit Score Seamlessly Every Month

Read Credit Report in Multiple Languages

How to Increase Your CIBIL Score Quickly and Effectively?

6 Steps-By-Steps Ways to Increase Your Credit Score from 600 to 750

The only way to rebuild and improve your CIBIL score online is through correcting any financial mistakes and making responsible choices in the future. Here are 6 proven methods you can employ to increase a low credit score naturally:

Step 1: Check Your CIBIL Report to Find the Root Cause

Your credit score by CIBIL is influenced by multiple factors and each factor requires a different remedial action. So, before taking any corrective action, the first step towards improving your CIBIL score should be to review your CIBIL report in detail to find the root cause.

Common reasons for a low CIBIL score include:

Once you identify which of these issues applies to you, you can work on improving your CIBIL score in a focused manner by taking the necessary steps to rectify the issue.

Avail Paisabazaar's Credit Health Pro Service to get personalized credit assistance. Our credit expert will call and analyze your credit report and suggest personalised solutions to build further or improve your credit score.

Step 2: Pay Your Dues Timely

If your low credit score is due to payment-related issues, then it is advised to address and resolve them first. Your payment history has one of the highest impacts on your CIBIL score as this lets the lenders know how likely you are to repay the borrowed money. Missed loan EMIs or delayed credit card bill payments are recorded in the Days Past Due (DPD) section of your credit report and stay for up to 36 months which negatively affects your score. Hence, to improve your CIBIL score, you can take the following measures:

Consistent on-time payments over the next few months can significantly help to improving your CIBIL score very fast & quickly.

If you tend to forget bill due dates, set standing instructions to auto-pay your bills as and when due or set reminders. A smart way to ensure timely credit card bill payment is to use Paisabazaar Bill Payment App where you can add all your credit cards and manage repayments easily. You receive alerts when a new statement is generated and when bills are due.

Read in Detail: Download Your CIBIL Report Online

Step 3: Reduce High Credit Utilisation

If you regularly max out your credit limit can make you look credit hungry and could lower your credit score. You may also struggle to make full repayment of your monthly card dues by the due date because of high credit usage. In such a case, reducing your credit utilisation ratio (CUR), that is the credit amount used in relation to the credit limit available, so that it stays within your monthly budget is recommended. A lower credit utilisation can signal a responsible credit behaviour and help boost your CIBIL score gradually.

To lower your CUR, avoid putting high-ticket purchases on your credit cards for some time. You can also request a limit increase on your credit cards or get a new credit card to increase your overall available limit. But be mindful that you do not utilise the additional limit.

Read in Detail: What is a Credit Score

Step 4: Limit Multiple Credit Applications Within A Short Duration

When you apply for a personal loan or credit card, the lenders initiate a hard enquiry on your credit profile, which can temporarily decrease your CIBIL score. However, multiple hard enquiries within a short time span can indicate credit-hungry behaviour and, as a result, lower your credit score. You must follow below mentioned steps to build your credit score:

Fewer credit enquiries help stabilise and improving your CIBIL score online.

There are two types of credit enquiries - soft enquiries and hard enquiries. When you check your own credit score to stay credit-aware, it is considered a soft-enquiry and has no impact on your credit score. In contrast, a hard enquiry is made when a lender or credit card issuer pulls your CIBIL report as part of a credit application.

Read in Detail: Credit Score Ranges

Step 5: Correct Errors in Your CIBIL Report

Even if you have maintained a good credit history, an error in your credit report that goes unnoticed can cause major damage to your credit score. This could include loans shown as active even after closure, incorrect personal information, wrong account details, mismatched overdue or paid-off amounts, duplicate accounts, etc. So, you must review your detailed credit health report every month on Paisabazaar Credit Score App, and if you spot any suspicious activity or discrepancy, follow the steps below:

Once the errors in your credit report are fixed, your CIBIL score can significantly improve automatically.

Avail Paisabazaar's Credit Health Pro Service for assistance in identifying errors in your credit report and to get them rectified at the earliest through our Credit Rectification Service.

Read in Detail: Found an Error in your Credit Report? Here's How to Raise a Grievance

Step 6: Build Credit If You Have Limited Credit History

Consumers with a longer credit history and a consistent record of timely repayments are trusted by the banks as well as bureaus. Hence, if you are new-to-credit or have a poor credit score, it is best to start as early as possible and build a positive track record to raise your CIBIL score by following the below-mentioned advice:

New-to-credit consumers or those with a poor credit score can get a secured credit card against FD to build or rebuild their score. A secured credit card is offered against a fixed deposit and hence approval is guaranteed. It works exactly like an unsecured card wherein you can make purchases and earn value-back in the form of rewards or cashback. Secured card activity is reported to credit bureaus and with responsible usage, you can improve your credit score.

Bottomline

Improving your CIBIL score fast is not possible through quick shortcuts, rather it requires identifying the root cause and taking targeted corrective steps to rectify the issues hurting your credit score. Moreover, this process is not instant and visible improvement can take few months of corrective action. More severe issues, like defaults or settlements may take longer, but consistent discipline always works in your favour. Therefore, you should check your free credit score regularly to understand your score improvement trajectory. You can witness the credit score improving from 600 to 800 if the pointers mentioned above are followed in a disciplined manner.

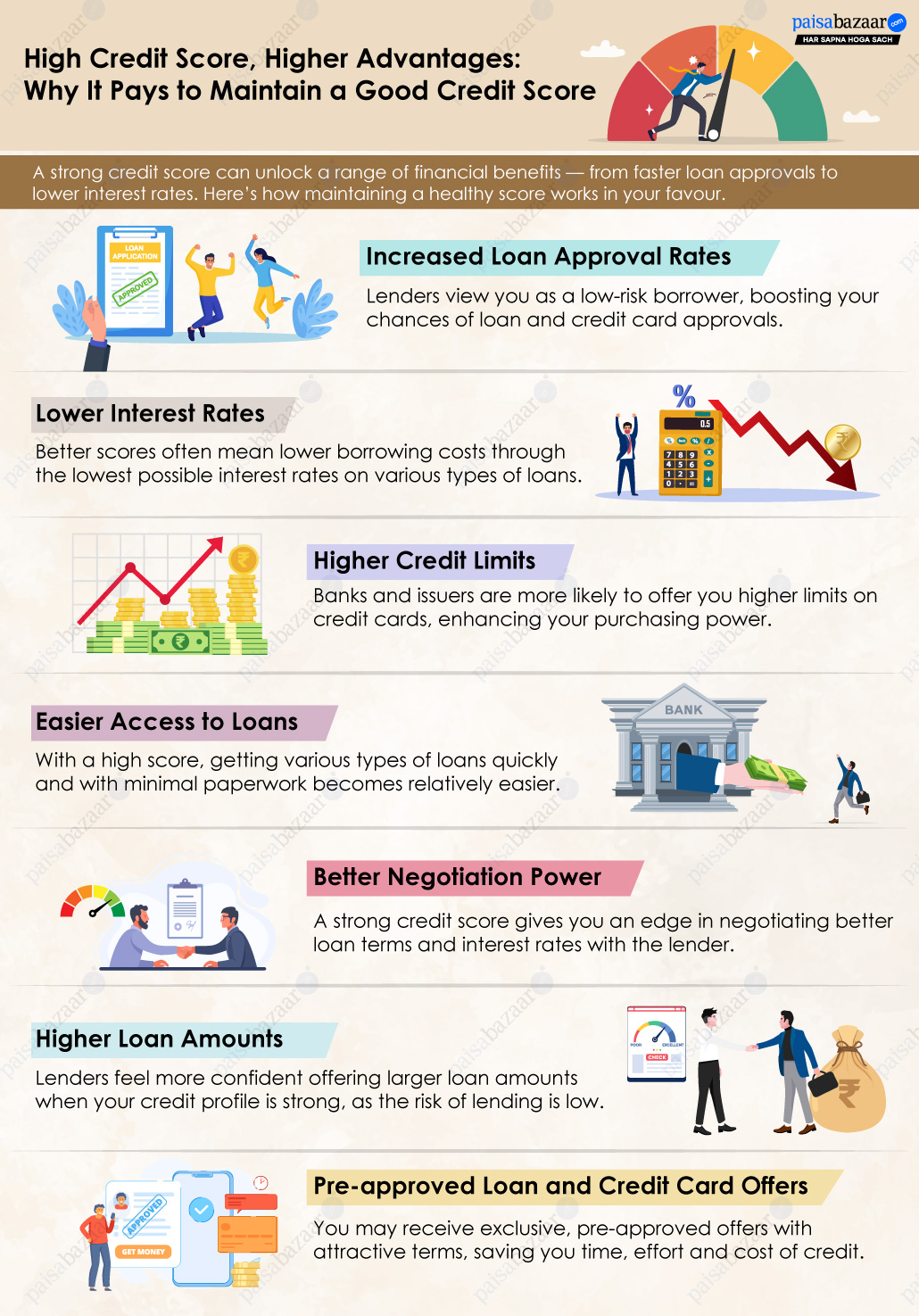

A better CIBIL score doesn't just improve loan approvals but also helps you secure lower interest rates, higher credit card limits, and faster approvals in the long run for instant business loan. Whereas a low credit score can act as a major hindrance for those looking for credit urgently.

How to Check CIBIL Score for Free with Paisabazaar?

Step 1: Enter your mobile number

Step 2: Verify your number using the OTP

Step 3: Enter your PAN and basic details

Step 4: View your free credit score and get detailed credit report

How to Check CIBIL Score for Free with Paisabazaar?

Step 1: Enter your mobile number

Step 2: Verify your number using the OTP

Step 3: Enter your PAN and basic details

Step 4: View your free credit score and get detailed credit report

FAQs

What is a good credit score?

A credit score above 750 is generally considered good and improves your chances of approval for loans and credit cards.

What is the fastest way to improve my credit score?

When it comes to credit score improvement, the quickest wins come from first identifying the cause of reduced score and then employing targeted remedial measures. For instance, if your credit score is low due to delayed payments then paying off your dues in full timely month over month would be the best step to take after clearing off any outstanding balance. Also, avoid maxing out your credit cards as this may signal irresponsible credit behaviour to the bureaus.

Does checking my credit score reduce it?

No, checking your own credit score is considered soft enquiry and has no impact on your credit score.

Should I pay the minimum due on my credit card to maintain a good credit score?

When you pay the minimum due on your credit cards on or before the due date, it is not considered as late payment and helps your credit score. However, it is not ideal as minimum payment leads to hefty interest charges on the unpaid amount as well as new purchases until the amount is paid off in full.

Can I build my credit score without a credit card?

Yes, while credit cards are the most popular first credit building product for many individuals, you can also build your credit score with other products, like personal loans, car loans, home loans, etc.

How to increase CIBIL score in 30 days?

Credit scores improve gradually and you may not see a significant jump in your CIBIL Score in 30 days. You should continue making timely payment of your credit card dues and loan EMIs, reducing your CUR and avoiding multiple credit applications within a short span. However, you might see a good jump if you had an error in your credit report and got it rectified.

Which are the best Secured Credit Cards to build Credit Score faster?

Secured credit cards are ideal for people with bad credit or new-to-credit consumers looking to build their credit score. Some of the best secured credit cards with low FD requirements are SBM Bank Paisabazaar Paisa+ Credit Card, SBM ZET Credit Card, IDFC FIRST Earn Credit Card, Utkarsh Super Money RuPay Credit Card and AU Nomo Credit Card.

Can I improve my score if I’ve defaulted on a loan before?

Yes, with consistent responsible credit behaviour, it is possible to improve your credit score even after a loan default. However, you should note that loan defaults remain on your credit profile for several years and your credit score may take a long time to show improvement. Start by clearing your past dues and continuously making bill payments timely.

How to Improve CIBIL Score before Applying for a Loan?

If you have a below average credit score and want to apply for a loan, you should immediately start working on credit score improvement. Pay off outstanding bills, reduce CUR and avoid multiple credit applications for at least 6-12 months before you plan on getting a new loan. A stable repayment history and lower debt levels will improve your chances of loan approval.

Does increasing my credit card limit help my score?

Yes. Increasing the credit limit on your existing credit cards helps reduce the overall credit utilization ratio (CUR), which favourably impacts your CIBIL Score. However, this will be helpful only if you keep the additional limit unutilised and continue paying off your bills on time.

Credit Score Articles

Delayed Credit Score Correction? RBI’s Compensation Framework Explained

Sumit Kumar12 Jun 2026

Does the Length of Your Credit History Affect Your Credit Score

Vandana Punj27 May 2026

I Have 4 Credit Cards and 2 Loans: How to Maximize My Credit Score?

Lepakshi Phogat26 May 2026

How to Manage Multiple Loans Without Hurting Your Credit Score

Neha Singh18 May 2026

How Can Students Build Their Credit Scores Without Income Proof?

Bharti18 May 2026

How Self-Employed Can Build Credit Score

Rupanshi Thapa12 May 2026

How Credit Utilization Ratio Works and What Percentage Should I Maintain

Sushmita Mishra12 May 2026

Why Did My CIBIL Score Drop Without any Reason?

Arvind Kumar08 May 2026

Why Minimum Due Payments Hurt Your Credit Score

Shruti Sharma06 May 2026

Not All Accounts Count: What Impacts Your Credit Score—and What Doesn’t

Samridhi Srivastava05 May 2026

Paisabazaar is a loan aggregator and is authorized to provide services on behalf of its partners

*Applicable for selected customers

Check Credit Score for FREE