Bonds are fixed income instruments, which the governments and entities issue to raise money for financing their projects, expenditures and other activities. In this, the investor purchasing bonds in India basically lends money to the bond-issuing entity. In return, the entity pays interest at periodical intervals (typically monthly/quarterly). When the bond reaches its maturity date, the bondholder gets back the principal value (face value) of the bond. Thus, bondholders can be considered as creditors for the bond issuers.

BondsWhat are BondsWhy Invest in BondsBonds Interest RatesTypes of BondsHow are Bonds Rated ?Benefits of Investing in BondsThings to Consider before Investing in BondsPaisabazaar in NewsFAQs

Bonds in India

Bonds in India can be a great option for earning stable returns. Start investing with just Rs. 1,000 and earnmonthly/ quarterly interest at Paisabazaar....

High returns

Earn fixed returns of up to 13.25%

Low investment

Start investing with as little as ₹1,000

Low risk

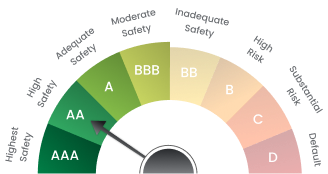

Invest in AAA–BBB rated bonds

No brokerage

0% brokerage or commission fees

4.5/5

15.6L Reviews

5.7cr+Satisfied Customers

₹3,064 CrsInvestment Enabled

100+Bonds

Invest as Low as ₹1000 & Getup to 13.25% Returns

High returns

Earn fixed returns of up to 13.25%

Low investment

Start investing with as little as ₹1,000

Low risk

Invest in AAA–BBB rated bonds

No brokerage

0% brokerage or commission fees

4.5/5

15.6L Reviews

5.7cr+Satisfied Customers

₹3,064 CrsInvestment Enabled

100+Bonds

Explore Bonds by Category

High Yield

INFOMERICS BBB

You Invest

₹9,922

Returns (YTM)

13.65%

You Get

₹11,928

Today

35 months

Best Capital Mar'29

You Invest

₹9,922

Returns (YTM)

13.65%

You Get

₹11,928

Today

35 months

Best Capital Mar'29

INFOMERICS BBB

ICRA BBB

You Invest

₹9,912

Returns (YTM)

13.25%

You Get

₹11,299

Today

13 months

Invest in Tencent Backed, Digitally-Driven NBFC Managing an AUM of 1,700+ Cr

You Invest

₹9,912

Returns (YTM)

13.25%

You Get

₹11,299

Today

13 months

Invest in Tencent Backed, Digitally-Driven NBFC Managing an AUM of 1,700+ Cr

ICRA BBB

IND BBB+

You Invest

₹9,826

Returns (YTM)

13.25%

You Get

₹11,425

Today

18 months

Gold Loan Backed Bonds of a Bharat Focused NBFC Managing 2,700+ Cr AUM

You Invest

₹9,826

Returns (YTM)

13.25%

You Get

₹11,425

Today

18 months

Gold Loan Backed Bonds of a Bharat Focused NBFC Managing 2,700+ Cr AUM

IND BBB+

What are Bonds?

How to Buy Bonds through Paisabazaar?

Get up to 13.25% from bonds in 5 simple steps

Step 1: Login to your Paisabazaar account

Step 2: Select the Bonds

Step 3: Complete the KYC process

Step 4: Enter bank details

Step 5: Link your demat account

Types of Bonds

Corporate Bonds

Listed public sector and private sector companies issue corporate bonds for financing their operations, expansion, debt consolidations, etc.

Central Government Bonds

Central government issues these bonds for tenures of 5 to 40 years with their interest payments at half yearly intervals.

Zero Coupon Bonds

These bonds do not offer any coupon (interest) payments to investors.

Capital Gains Bonds

These bonds help individuals and Hindu Undivided Families (HUFs) save on Long-Term Capital Gains (LTCG) tax liability arising from the sale or transfer of their land or building.

Floating Rate Bonds

The interest or coupon payments of these bonds are linked to predetermined benchmark rates, which if changes could also change the bond’s coupon rate.

State Development Loans (SDL)

State governments in India issue State Development Loans (SDLs). They are almost as secure as Central Government Bonds.

Municipal Bonds

Urban local bodies issue municipal bonds to raise money for financing various development projects.

Convertible Bonds

These bonds can be converted into shares after a specified period, either at the current market price or at a price pre-determined at the time of the bond issue.

Callable Bonds

In these bonds, issuers have the right to buy back these bonds before their maturity dates.

Bonds Interest Rates

Bonds interest rate is the interest rate a bond issuer promises to pay on a bond’s face value. More simply, it is the amount bondholders receive periodically on their bond investment. So, let’s say if a bond has a face value of Rs 100 and a interest rate of 8.24%, then the annual coupon (interest earnings) would be Rs. 8.24.

Based on coupon rate, bonds are categorised as fixed rate bond and floating rate bonds. In case of fixed rate bonds, the interest payments remain fixed or unchanged till the bond’s maturity date. However, in case of floating rate bonds, the coupon rate is reset at predefined intervals and is based on a pre-specified market-based interest rate. Thus, interest payments may vary during the bond tenure.

Why Invest in Bonds through Paisabazaar?

High Returns

Earn fixed returns of up to 13.25%.

Low Risk

Invest in a range of highly rated (AAA-BBB) corporate bonds.

Flexible Payout

Get fixed returns credited in your demat linked bank account every month/ quarter.

Low Investment

Start investing with as little as Rs. 1,000.

Safety & Security

Invest in SEBI-regulated senior secured bonds to enjoy higher claim priority over shareholders in case of default or liquidation.

Sell Anytime

Sell bonds anytime through Paisabazaar.

Transparency

Real-time price discovery and assured transaction.

No brokerage/commission

Invest without paying brokerage or commission fee.

End-to-end digital process

Enjoy seamless end-to-end digital process.

Bonds Video Tutorials

People also search for

How are Bonds Rated?

6 Benefits of Investing in Bonds in India

Bonds offer several key benefits, including steady income generation, capital preservation, and portfolio diversification, making them a cornerstone of a balanced investment strategy.

Steady Income Stream:

Bonds usually offer fixed interest at regular intervals, providing investors a steady income stream.

Capital Preservation:

The principal of bonds is repaid at maturity, making them ideal for those seeking capital protection amid market volatility.

Diversification:

Investing in bonds can offset the risks associated with more volatile assets like stocks.

Lower Volatility:

Bonds usually show lower price volatility than stocks, offering stability to risk-averse investors.

Predictable Returns:

Bonds offer fixed interest and guarantee to return the principal at maturity, helping investors estimate their future returns and plan their finances in advance.

Potential for Capital Gains:

Investors usually hold bonds for income, however, they can also provide profits if they are sold at higher prices before maturity.

Things to Consider before Investing in Bonds

Here are a few points that investors should consider before investing in bonds in India:

Paisabazaar Bonds in News

How to Buy Bonds through Paisabazaar?

Get up to 13.25% from bonds in 5 simple steps

Step 1: Login to your Paisabazaar account

Step 2: Select the Bonds

Step 3: Complete the KYC process

Step 4: Enter bank details

Step 5: Link your demat account

FAQs

Bonds Articles

How NRIs Can Invest in Corporate Bonds

Paisabazaar31 Mar 2026

Digital Gold vs SGB

Paisabazaar10 Mar 2026

Bonds vs Mutual Funds – Which Investment Option is Right for You?

Paisabazaar25 Feb 2026

Sovereign Gold Bond vs Gold ETF – Which is Better?

Paisabazaar24 Feb 2026

Convertible Bond vs Non-Convertible Bonds

Paisabazaar13 Feb 2026

How to Invest in Government Bonds

Paisabazaar12 Feb 2026

How Corporate Bond Works

Paisabazaar10 Feb 2026

Deep Discount bonds vs Zero Coupon Bonds

Paisabazaar06 Feb 2026

Bonds vs Stocks

Paisabazaar14 Jan 2026

Advantages and Disadvantages of Sovereign Gold Bonds

Paisabazaar10 Dec 2025

Written By

Vandana PunjReviewed By

Shamik GhoshCheck Top Bond Offers with Assured Returns of up to 13.25%

Paisabazaar is a loan aggregator and is authorized to provide services on behalf of its partners

*Applicable for selected customers