Download the

Paisabazaar app Today!

Paisabazaar app Today!

Get instant access to loans, credit cards, and financial tools — all in one place

Get the app — instant card and loan offers!

Our Advisors are available 7 days a week, 9:30 am - 6:30 pm to assist you with the best offers or help resolve any queries.

Get instant access to loans, credit cards, and financial tools — all in one place

Scan to download on

Our Advisors are available 7 days a week, 9:30 am - 6:30 pm to assist you with the best offers or help resolve any queries.

Table of Content:

A Systematic Investment Plan (SIP) is an alternative to the traditional lump sum mode of investment. Under a SIP, a certain amount is deposited in a mutual fund scheme at periodic intervals. A SIP helps an investor to benefit from the power of compounding and rupee cost averaging while keeping the periodic investment requirement light on the pocket as a SIP can be started with an amount as low as Rs. 100 or Rs 500.

Each time an investor makes a payment, the fund manager purchases more units of the assets (shares and securities) of the firms the fund is invested in. This gradually increases the number of units owned by the investor and hence SIPs are suitable for the long term. There are several advantages of investing through SIP as explained next.

SIPs allow investors to invest with amounts as low as Rs. 100 or 500 at regular intervals. This helps them to invest without any financial burden as well as reduces the financial risk associated with lump sum investments.

Through SIP, one invests periodic amounts instead of a larger sum. The fund manager can purchase more units of market-linked instruments (equities and debt) every time. More units are bought when stock prices are low and vice versa. Thus, a SIP enables you to lower the average cost of your investment and reduce the risk associated with market volatility by spreading the purchase price over time. This is known as rupee cost averaging

A SIP enables you to regularly increase your investment amount by a fixed amount. The returns are calculated on the amount invested plus the previous returns. Thus, the returns are compounded and this is the power of compounding of a SIP.

Also Know: How to Compare Two Mutual Funds

Considering the above mentioned advantages, it is beneficial to stay invested through SIP mode of mutual fund investment. Also, SIP mode is light on pocket and investors with low monthly salary can also invest in mutual funds.

SIP can be adopted as a way of payment for any mutual fund. Listing down best mutual funds for SIP for FY 2020:

| Fund Name | 3 Year Returns (%) | 5 Year Returns (%) |

| ICICI Prudential Bluechip Equity Fund | 21.37 | 18.03 |

| IIFL Focused Equity Fund | 18.9 | 16.92 |

| Invesco India Financial Services Fund | 14.18 | 16.86 |

| Axis Bluechip Fund | 17.69 | 16.45 |

| PGIM Global Equity Opportunities Fund | 23.27 | 16.32 |

| Axis Focused 25 Fund | 15.13 | 16.25 |

| Axis Small Cap Fund | 17.67 | 16.16 |

| ABSL Digital India Fund | 18.52 | 16.07 |

| Mirae Asset Emerging Bluechip Fund | 11.66 | 15.36 |

| SBI Focused Equity Fund | 15.24 | 15.22 |

(3 year/5 year returns are annualized. These are the best SIPs to invest as per the data based on 5 Year SIP Returns of schemes as on February 19, 2020, Source: Value Research)

Also Read : Best SIP investments for 2020

The tax on SIPs depends on the nature of the mutual fund scheme – equity or non-equity. You can read about the tax treatment of equity and non-equity mutual funds here.

Mostly SIPs are used for equity funds and as per tax rules of all equity funds, capital gains up to Rs. 1 Lakh (after 1 year) are exempted from taxation, and the rest are taxed at 10% as per the taxation norms of Equity Funds. For example, an investor makes capital gains of Rs. 2 Lakh, then Rs. 1 Lakh is exempted from tax and the remaining Rs. 1 Lakh will be taxed at 10%. Thereby, the payable tax at remaining rs. 1 Lakh is Rs. 10,000.

If the s/he redeems the fund in less than a year (ELSS are locked in for 3 years), then the capital gains will be taxed at 15% and no tax exemption will be provided. In that case, the payable tax on Rs. 2 Lakh of gains would be Rs. 30,000.

You can fill forms and update the bank for money deduction of a certain amount on a certain date of every month for SIP of an mutual fund scheme.

For detailed information on how to invest in mutual funds, click here

Be mindful of the following mistakes while making a SIP mutual fund investment so that you can create and appreciate your wealth to maximum levels:

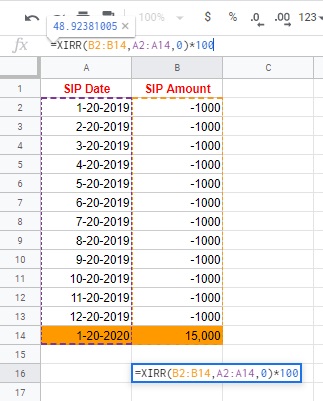

Let’s assume you invested ₹1,000 every month on a particular date in a mutual fund scheme through SIP. If you started investing in January 2019, then you have already invested ₹12,000 till December. For instance, you checked the market value of your units through investments on January 20, 2020 that stands out as ₹15,000. It means you have earned a return of 48.92% on your invested money.

*There is a minus(-) sign in front of ₹1,000 as it is the cash outflow (which you will be investing) every month whereas there’s no such sign in front of ₹15,000 because that is the amount you will get if you redeem the plan.

Suggested Read: SIPs and Market Correction: What you should know?

Q. What if I miss a SIP installment?

A. In case you miss a SIP installment or two, you will neither be charged extra nor your plan will be discontinued. You can miss up to 3 installments. Automated SIP installment may get missed because of low account balance. In this case, banks may charge for not maintaining minimum balance. Some AMCs allow the option of pausing SIP installments for about a few months (3 to 6) for some schemes.

Q. Do all investments through SIP have tax benefits?

A. No, it depends on the scheme. Not all mutual fund schemes are Tax Saver Plans and hence not all SIPs have tax benefits. Tax Saver SIPs also known as Equity Linked Saving Schemes (ELSS) are the only SIP plans with tax saving benefits under Section 80C of the Income Tax Act. It also comes with a lock-in period of 3 years.

Q. Can I withdraw from an ELSS SIP before 3 years?

A. No, you can’t withdraw from ELSS before 3 years. Money from other SIPs who don’t have a lock in period can be withdrawn.

Q. Which SIP is best for 5 years?

A. Any plan outperforming in the market can be considered for SIP. Table given in the article above lists the best mutual fund schemes based on 5 Year Returns on a certain date.

Q. What is NAV in SIP?/

A. NAV – Net Asset Value is the cost of one unit of a fund’s shares. It is calculated as the difference between the fund’s total assets and its liabilities, divided by the total number of shares.

Q. Can I reduce my SIP amount or increase my duration?

A. Yes. Both are possible. After the completion of tenure of the SIP, it can be extended. Also, there are various types of SIPs as explained above where investors have the option to periodically increase or rather change the installment amount as per the need. It depends on the fund scheme.

Q. What is a Flexi SIP?

A. A Flexi SIP is the one which allows you to change the amount of your investments every month. If you don’t want a fixed amount of installment and want more control over it, you can set up a Flexi SIP. You need to specify a default amount for your investments.

Q. What is the best time to start SIP?

A. There is no such fixed time but as soon as you become a salaried person, it is suggested to invest at least 1/10th of your salary in SIP. Market conditions keep changing and hence it is always recommended to stay invested for long.

Also Check: Smart SIP

In order to be a successful investor, it is paramount that investments are made in a systematic manner and this is where the SIP calculator provided by Paisabazaar.com can play a key role. A prospective investor can use a SIP calculator to figure out how much his/her investment will grow at the end of a specific tenure for a specific amount. Alternately, if the investor has a fixed goal in mind such as a corpus for retirement or buying a house, a SIP calculator can help him/her find out how much monthly investment is required in order to achieve that corpus timely.