Download the

Paisabazaar app Today!

Paisabazaar app Today!

Get instant access to loans, credit cards, and financial tools — all in one place

Win Assured Cashback

Our Advisors are available 7 days a week, 9:30 am - 6:30 pm to assist you with the best offers or help resolve any queries.

Get instant access to loans, credit cards, and financial tools — all in one place

Scan to download on

Our Advisors are available 7 days a week, 9:30 am - 6:30 pm to assist you with the best offers or help resolve any queries.

Check Free Credit Score & Win up to ₹1 lakh

Let’s Get Started

The entered number doesn't seem to be correct

| To invest in NPS through Paisabazaar, Click Here |

| Already have an NPS account through us? For Subsequent Contribution, Click Here To Set up SIP, Click Here |

Note: The information on this page may not be updated. For latest information, click here.

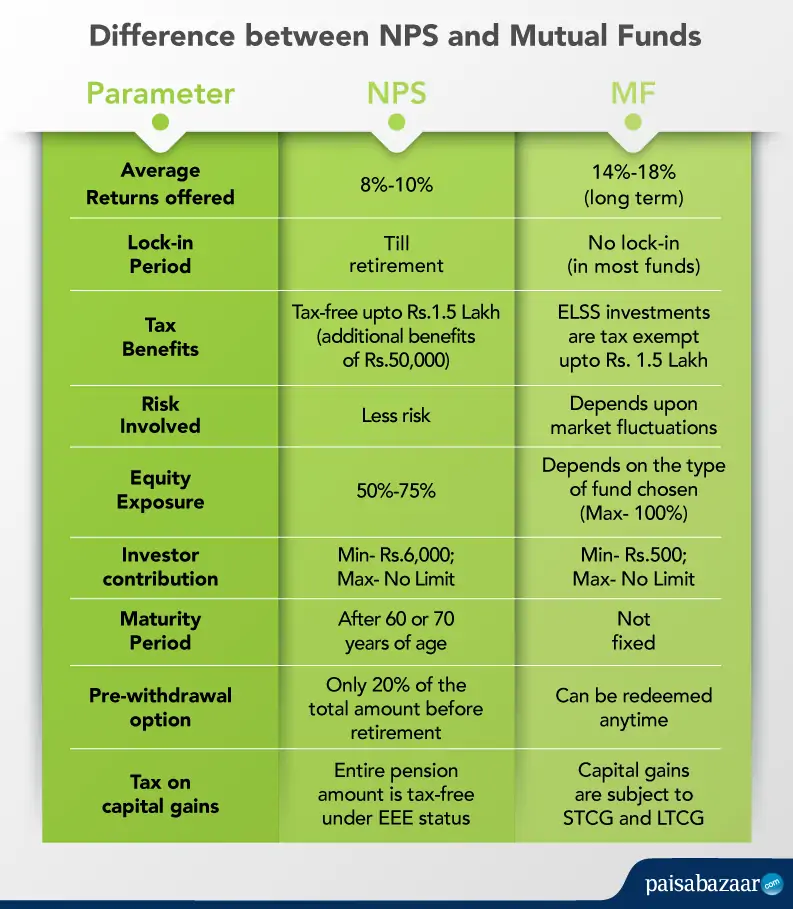

NPS is a type of investment that working individuals may choose to lock in their funds for the purpose of safe retirement. On the other hand, Mutual Funds are open-ended, professionally managed investment options that pool in money from multiple investors to purchase securities. However, both are market-linked investment plans.

National Pension System and Mutual Funds, both allow investors to pool in their funds at fixed, regular intervals (in case you choose to invest via SIP) for the long term. It must be noted that many investors equate SIPs to mutual funds and use them interchangeably. Whereas, SIPs (Systematic Investment Plans) are a way of investing in Mutual Funds (that are an investment option for investors).

It is of importance that you understand both the investment options before making a choice of where and how to invest. Let’s first learn about the National Pension System and Mutual Funds as individual investment options.

Table of Contents :

A social security initiative launched by the central government, National Pension System is a pension plan launched in January 2004 for the financial welfare of the employees working in the government sector. Eventually, by the year 2009, the scheme was made available to all the working professionals. NPS is popular as a retirement scheme and for the tax benefits that come with it.

Also Read: All that you should know about NPS

Mutual Funds can be referred to as a basket of multiple and varied financial instruments that generate returns over a long period of time. Experienced professionals, called fund managers, are appointed by AMCs to carefully administer the funds of investors and change allocations according to the fluctuations in the market.

Learn more about Mutual Funds here.

Based on the allocation of their assets, Mutual funds can majorly be classified into the following 3 categories-

It must be noted that while investing in mutual funds, investors have a choice of investing via SIPs or Lump sum, depending on their own ease.

Suggested Read: Lump sum vs SIP mode of investing in mutual funds

As you decide which mutual fund to invest in, You must also go through the returns delivered by any fund in the past. Additionally, it is advised that you have a fair idea of how much returns to expect in a given time period. To do so, you can use the Mutual Fund Calculator before making the choice.

Read More: List of Top Ranked Mutual Funds

When it comes to choosing between the given investment options, both NPS and Mutual Funds instill a sense of financial discipline in your life as the amount gets debited from your registered account at pre-defined intervals automatically (especially if invested via the SIP mode).

Mutual Funds, in most cases, also act as emergency funds because of the level of flexibility offered by them. You can choose to withdraw your funds (with no or some exit load based on the scheme). Hence, it is advised to invest in NPS when retirement, along with tax benefits is your goal, and you have a less risk appetite.

Additionally, you can also save on taxes during the period of your employment as NPS offers a tax deduction of upto Rs.1.5 Lakh for your and your employer’s contribution to the scheme, under Section 80CD of the Income Tax Act. Moreover, you can also claim any additional self contribution (up to Rs.50,000) to the scheme under Section 80CCD as NPS tax benefit.

Along with this, NPS was put into the EEE (Exempt-Exempt-Exempt) category in the 2019 budget. This implies that NPS subscribers can claim tax deductions on NPS contributions, returns earned on the NPS contributions are also tax exempt and with tax benefits extended on lump sum withdrawal, NPS now qualifies to be an Exempt-Exempt-Exempt (EEE) category product. On the other hand, capital gains in Mutual funds are subject to short term and long term taxation.

Given their similarities and differences, you should make a wise choice between both the investment options depending upon your financial objectives. If the main motive behind investing is to secure your retirement financially, NPS should be your choice. Mutual Funds are generally popular for individuals who have a high risk appetite, may have short-term financial goals and can also serve other goals.

Mutual fund investments via SIP allow investors to register an auto-debit mandate with their banks. This allows them to stay away from the hassle of paying their SIP amount every week/month/quarter/year as the process gets done automatically.

However, if you decide to invest in NPS, you can still choose to invest via the SIP mode either manually or using the auto-debit option. You can use the manual option to pay your SIP installment if your bank does not offer an auto-debit feature through the online portal.

On the other hand, you can opt for the auto-debit feature by notifying your bank about your NPS investment in NPS. Additionally, investors in the NPS Corporate Model and the Government Model have a fixed amount deducted from their salaries every month and get it invested in NPS, which automatically acts as an SIP.