Download the

Paisabazaar app Today!

Paisabazaar app Today!

Get instant access to loans, credit cards, and financial tools — all in one place

Win Assured Cashback

Our Advisors are available 7 days a week, 9:30 am - 6:30 pm to assist you with the best offers or help resolve any queries.

Get instant access to loans, credit cards, and financial tools — all in one place

Scan to download on

Our Advisors are available 7 days a week, 9:30 am - 6:30 pm to assist you with the best offers or help resolve any queries.

Your CIBIL score is the first factor that lenders check to assess your creditworthiness and determine the chance of approval of your application for loan or a credit card. If your CIBIL score is low, banks and NBFCs are likely to reject your application which can further impact your credit profile negatively. This can make it difficult for you to access any kind of credit, thus limiting your credit opportunities. Moreover, even if your credit application is accepted, the loan offer might come at a higher rate of interest.

However, you can still rebuild a low CIBIL score by identifying the factors responsible for the drop in your score. Employing targeted corrective measures and an overall disciplined financial behaviour can help you improve your CIBIL score by undoing any damage caused by past actions.

How to Improve Your CIBIL Score: Snapshot

|

The only way to rebuild and improve your CIBIL score is through correcting any financial mistakes and making responsible choices in the future. Here are some of the steps you can employ to improve a low CIBIL score:

Your credit score by CIBIL is influenced by multiple factors and each factor requires a different remedial action. So, before taking any corrective action, the first step towards improving your CIBIL score should be to review your CIBIL report in detail to find the root cause.

Common reasons for a low CIBIL score include:

Once you identify which of these issues applies to you, you can work on improving your CIBIL score in a focused manner by taking the necessary steps to rectify the issue.

Avail Paisabazaar’s Credit Health Pro Service to get personalized credit assistance. Our credit expert will call and analyze your credit report and suggest personalised solutions to build further or improve your credit score.

If your low score is due to payment-related issues, then it is advised to address and resolve them first. Your payment history has one of the highest impacts on your CIBIL score as this lets the lenders know how likely you are to repay the borrowed money. Missed loan EMIs or delayed credit card bill payments are recorded in the Days Past Due (DPD) section of your credit report and stay for up to 36 months which negatively affects your score. Hence, to improve your score, you can take the following measures:

Consistent on-time payments over the next few months can significantly improve your CIBIL score.

If you tend to forget bill due dates, set standing instructions to auto-pay your bills as and when due or set reminders. A smart way to ensure timely credit card bill payment is to use Paisabazaar App, where you can add all your credit cards and manage repayments easily. You receive alerts when a new statement is generated and when bills are due.

If you regularly max out your credit limit can make you look credit hungry and could lower your credit score. You may also struggle to make full repayment of your monthly card dues by the due date because of high credit usage. In such a case, reducing your credit utilisation ratio (CUR), that is the credit amount used in relation to the credit limit available, so that it stays within your monthly budget is recommended. A lower credit utilisation can signal a responsible credit behaviour and help boost your CIBIL score gradually.

To lower your CUR, avoid putting high-ticket purchases on your credit cards for some time. You can also request a limit increase on your credit cards or get a new credit card to increase your overall available limit. But be mindful that you do not utilise the additional limit.

When you apply for a new loan or credit card, the lenders initiate a hard enquiry on your credit profile, which can temporarily decrease your CIBIL score. However, multiple hard enquiries within a short time span can indicate credit-hungry behaviour and, as a result, lower your credit score. So, to improve your score:

Fewer credit enquiries help stabilise and improve your CIBIL score.

There are two types of credit enquiries – soft enquiries and hard enquiries. When you check your own credit score to stay credit-aware, it is considered a soft-enquiry and has no impact on your score. In contrast, a hard enquiry is made when a lender or credit card issuer pulls your CIBIL report as part of a credit application.

Even if you have maintained a good credit history, an error in your credit report that goes unnoticed can cause major damage to your credit score. This could include loans shown as active even after closure, incorrect personal information, wrong account details, mismatched overdue or paid-off amounts, duplicate accounts, etc. So, you must review your detailed credit report every few months, and if you spot any suspicious activity or discrepancy, follow the steps below:

Once the errors in your credit report are fixed, your CIBIL score can improve automatically.

Avail Paisabazaar’s Credit Health Pro Service for assistance in identifying errors in your credit report and to get them rectified at the earliest through our Credit Rectification Service.

Read in Detail: Found an Error in your Credit Report? Here’s How to Raise a Grievance

Consumers with a longer credit history and a consistent record of timely repayments are trusted by the banks as well as bureaus. Hence, if you are new-to-credit or have a poor credit score, it is best to start as early as possible and build a positive track record to raise your CIBIL score by following the below-mentioned advice:

New-to-credit consumers or those with a poor credit score can get a secured credit card against FD to build or rebuild their score. A secured credit card is offered against a fixed deposit and hence approval is guaranteed. It works exactly like an unsecured card wherein you can make purchases and earn value-back in the form of rewards or cashback. Secured card activity is reported to credit bureaus and with responsible usage, you can improve your credit score.

Improving your CIBIL score is not possible through quick shortcuts, rather it requires identifying the root cause and taking targeted corrective steps to rectify the issues hurting your credit score. Moreover, this process is not instant and visible improvement can take 3 to 6 months of corrective action. More severe issues, like defaults or settlements may take longer, but consistent discipline always works in your favour. Therefore, you should check your credit score regularly to understand your score improvement trajectory. You can witness the credit score improving if the pointers mentioned above are followed in a disciplined manner.

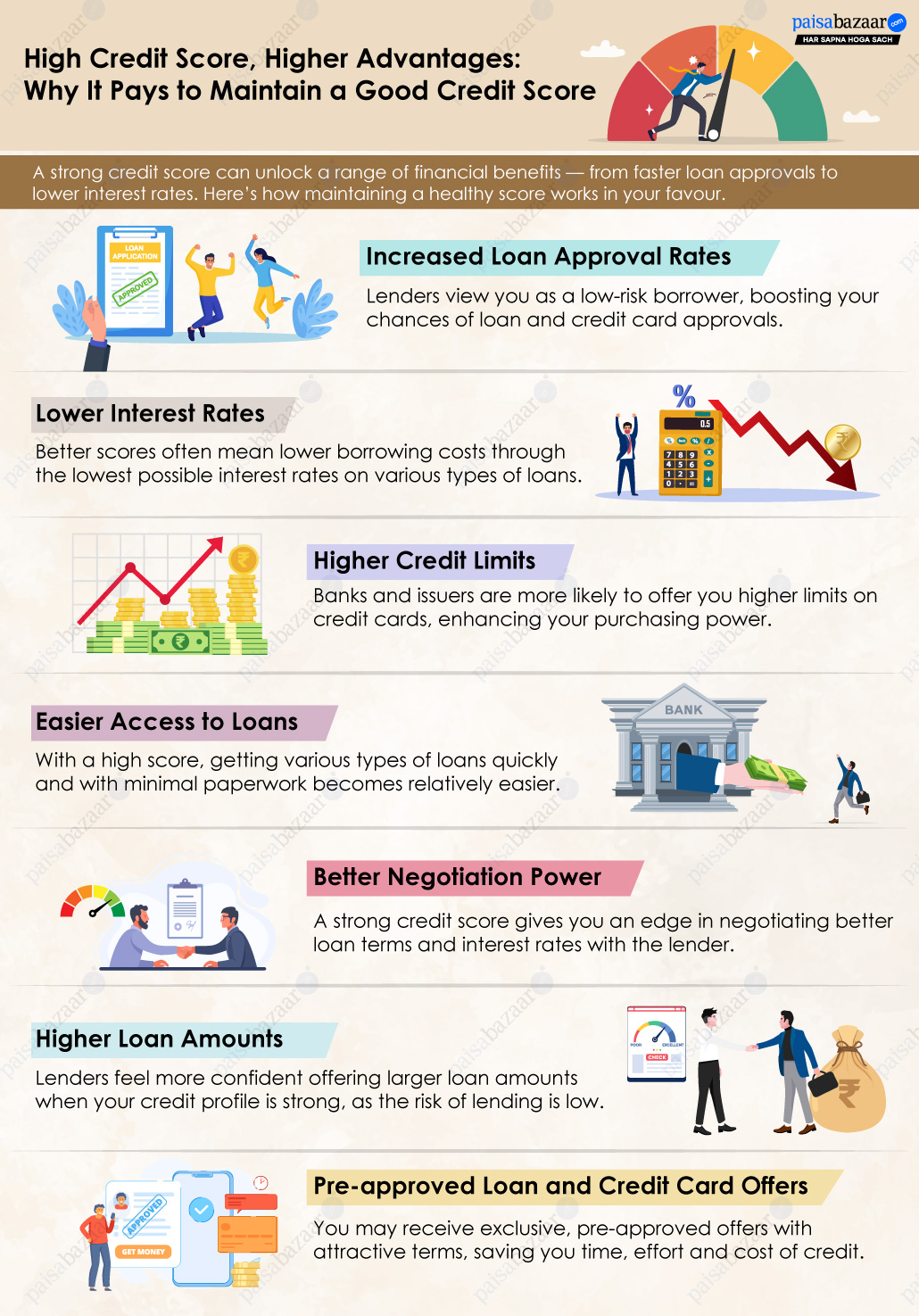

A better CIBIL score doesn’t just improve loan approvals but also helps you secure lower interest rates, higher credit limits, and faster approvals in the long run. Whereas a low credit score can act as a major hindrance for those looking for credit urgently.