Download the

Paisabazaar app Today!

Paisabazaar app Today!

Get instant access to loans, credit cards, and financial tools — all in one place

Win Assured Cashback

Our Advisors are available 7 days a week, 9:30 am - 6:30 pm to assist you with the best offers or help resolve any queries.

Get instant access to loans, credit cards, and financial tools — all in one place

Scan to download on

Our Advisors are available 7 days a week, 9:30 am - 6:30 pm to assist you with the best offers or help resolve any queries.

Check Free Credit Score & Win up to ₹1 lakh

Let’s Get Started

The entered number doesn't seem to be correct

Tax audit, as mentioned in section 44AB of the Income tax Act, needs to be conducted by a professional auditor approved by the Income Tax Department. This professional could be a Chartered Accountant (CA) having a full-time certificate of professional practice or a company specialising in this field. The tax audit ensures the accuracy and correctness of the Books of Account owned and maintained by the taxpayers and that their income is calculated on the basis of the applicable Income Tax Rules. Form 3CB is one of the key forms which is used to submit an audit report generated u/s 44AB of the Income Tax Act, 1961.

This form is needed when the taxpayer who is working as a professional or a business does not need to get the book of accounts audited by law. When an individual, partnership firm or proprietorship entity has a turnover of over Rs. 1 crore and has not opting for the presumptive taxation scheme, there is no audit of books of account needed under any law apart from the Income Tax Act. For this, they have to furnish Form 3CB. In addition to Form 3CB, the tax auditor can furnish the Form 3CD as well.

Form 3CB is an audit report that is furnished by a professional CA on the behalf of the tax assessee who is working as a self-employed professional or carrying out a business. The assessee undergoing audit has to obtain the report in Form 3CB on or before September 30 of the applicable assessment year. For instance, if the relevant assessment year or financial year is 2017-18, then the audit report must be obtained by them until September 30, 2020.

Key fields in Form 3CB that must be filled out by the auditor after conducting the audit of the books of account under section 44AB are as follows:

The following are the key sections present in Form 3CB and key fields in each section:

Section 1

Section 2

Section 3 (a)

This section contains various observations, qualifications, comments and discrepancies observed during the audit.

Section 3 (b)

This section features the declaration provided by the auditor

Section 4

Section 5

Section 6

Get FREE Credit Report from Multiple Credit Bureaus Check Now

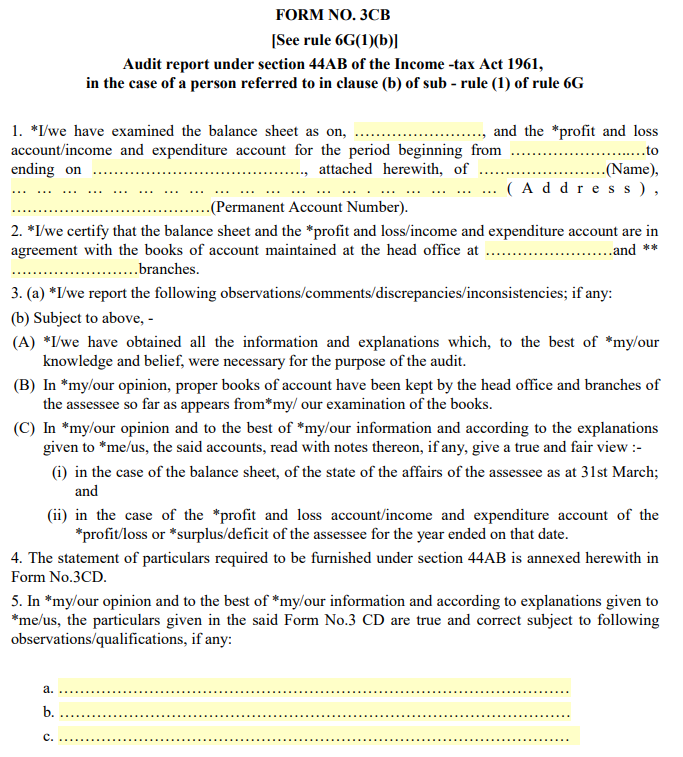

You can download Form 3CB for free from the Income Tax of India website. Subsequently the downloaded form can be printed, filled out and submitted with the appropriate authorities. The following is a sample Form 3CB:

What are the Key Differences between Form 3CA, 3CB and 3CD?

What are the Key Differences between Form 3CA, 3CB and 3CD?The key difference between Form 3CA and Form 3CB is with respect to the applicability. While Form 3CA needs to be submitted by individuals who are mandatorily required to be audited u/s 44AB of the Income Tax Act, Form 3CB is applicable to even those who are audited under other sections too. While both 3CA and 3CB are short single page forms, Form 3CD is a much more detailed document that shows details of the audit that was carried out by the auditor. Form 3CD operates as a supporting document that needs to be submitted with both Form 3CA and 3CB as proof of completion of a mandatory audit.