Download the

Paisabazaar app Today!

Paisabazaar app Today!

Get instant access to loans, credit cards, and financial tools — all in one place

Win Assured Cashback

Our Advisors are available 7 days a week, 9:30 am - 6:30 pm to assist you with the best offers or help resolve any queries.

Get instant access to loans, credit cards, and financial tools — all in one place

Scan to download on

Our Advisors are available 7 days a week, 9:30 am - 6:30 pm to assist you with the best offers or help resolve any queries.

Life is full of uncertainties, but you need to devise ways to manage the risks arising out of these issues. A life insurance policy is one such means of providing financial security to the family in case of any eventuality like the sudden demise of the breadwinner. To get the benefit when needed, you should know and understand life insurance plans & policies in India.

Life insurance provides financial protection to the family in cases like the sudden death or the permanent disability of the main earning member of the family. Thus, it is an assurance that the insurance company will take care of the financial well-being of the family members even when the breadwinner is not around. This is done by paying the sum assured to the nominee or the beneficiary. The insurance can also cover other contingencies like critical illness and permanent or temporary disability. The policyholder is called the insured, while the insurance company is called the insurer.

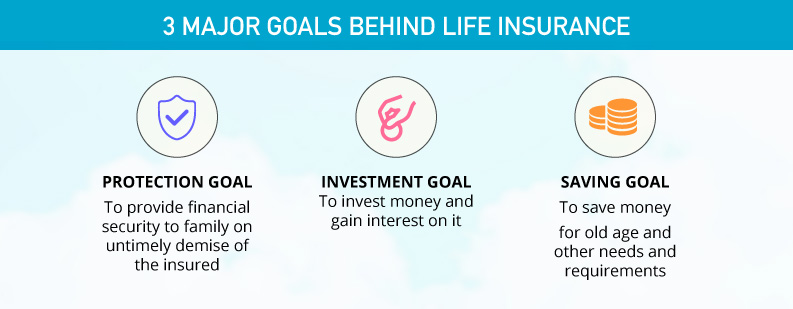

A life insurance policy helps in meeting three goals in life. Let us look at them:

A premium is the amount paid to the insurance company for getting a life insurance policy. The premium or the cost of the insurance is an important aspect to be considered before finalising a policy. It depends on various factors like age and gender. To reap the benefits of the insurance policy, it is important to pay the premium on time. In case of a non-payment or a payment delay, the policy can be considered as a lapsed policy. However, before a policy happens to expire, you usually get a grace period of 30 days. The payment mode can be regular or single. A regular payment can be monthly, annually and so on. Let us understand some factors on which the premium depends.

Age: This is an important deciding factor while buying an insurance policy. Older you are, higher the premium amount. Accordingly, younger people have to pay lower premium amount for a life insurance policy.

Gender: Premium amount for women is lower compared to that for men.

Smoker/Non-smoker: In case you are a smoker, the premium will be higher because you are prone to higher risks in life. Thus, a non-smoker has to pay lower premium.

Sum assured: Higher the sum assured or the death benefit, higher the premium amount to be paid.

Policy term: If the policy is for a longer duration, the premium amount will be higher.

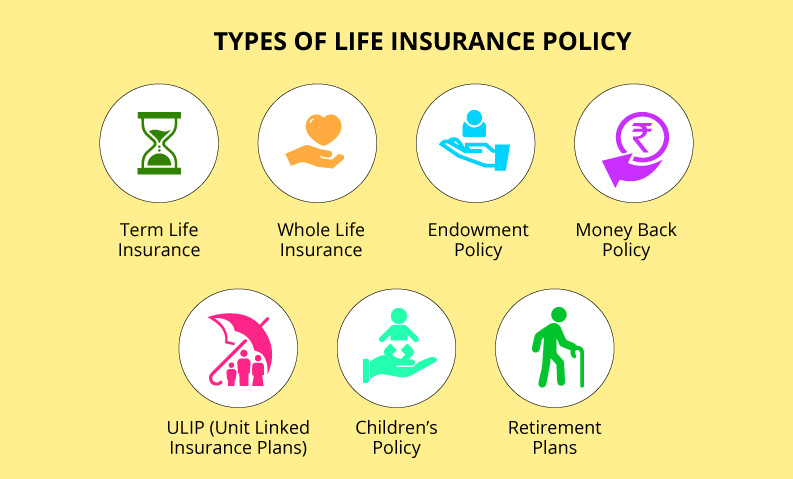

Life insurance is of 7 types. And each has its own features and specialties. You can choose them as per your need and requirement. They are: Term Insurance, Whole Life Insurance, Endowment Policy, Money Back Policy, Child Plan, Retirement or Annuity Plan and United Linked Insurance Plan (ULIP).

Term insurance is a pure protection plan where the beneficiary gets the sum assured, also called death benefit, if the policyholder passes away during the term of the plan. However, if the insured survives the term plan, the coverage also ends, with the beneficiary not getting any money. Even the premium paid is not refunded to the insured.

However, there are some term plans where the premium paid is returned, if the policyholder happens to the survive the plan. This payment is termed as survival benefit. The premium for such plans are quite high. Otherwise, a pure term plan is one of the most affordable plans compared to other types, as the amount of the premium is quite nominal. One can opt for regular payment or single payment mode.

| TYPES OF TERM INSURANCE | ||

| Level Term Insurance | Decreasing Term Insurance | Increasing Term Insurance |

| Sum assured for the beneficiary remains constant throughout the term of the plan. Even the premium and renewal premium remain same during the term | Sum assured decreases with time and the premium amount remains constant. Example: credit life insurance, mortgage redemption policies | Not just sum assured, but also premium amount increases with time |

Under this policy, the insured is covered for the lifetime, i.e. till his/her death. The maturity age is usually 100 years. Thus, you need to keep paying the premiums till 100 years of your age. Here, the beneficiary gets the sum assured along with maturity benefits on the untimely demise of the policyholder. On the other hand, the policyholder gets to enjoy the survival benefits, in case he/she happens to survive the policy term. A whole life insurance plan offers benefits in both the cases – when the policyholder survives the policy or on his/her sudden demise during the term.

This offers both coverage and a means for saving. Like any other life insurance plan, here, the beneficiary gets the sum assured in case of the death of the insured. However, if the insured survives the plan, he/she gets the maturity benefit. The policy can be both participating, where the insured gets bonus and dividends from the company, and non-participating, where the insured does not get bonus and dividends from the insurance company. An endowment policy can also be a ULIP, where a part of the premium is invested in market apart from a part being used in coverage.

In this policy, the insured gets a certain percentage of the sum assured at regular intervals during the term of the policy. If the insured survives the tenure of the policy, he/she also gets the sum assured irrespective of the percentage of the sum assured already paid out to him/her. Thus, at the end, the insured gets the sum assured along with the accumulated bonus.

And in case of the death of the insured during the term of the policy, the beneficiary gets the full sum assured regardless of the number of premiums paid. It is one of the expensive policies, as it provides benefit to the insured during the term period along with the long-term benefits of usual life insurance plans. A money back policy provides benefit to the insured in between the term of the insurance which he/she can use for meeting various financial goals.

People can take this insurance plan if they want to save money for the future of their child along with getting a coverage for the breadwinner. It is a combination of savings and insurance, where the insured can use the money for the future needs of the child like higher education. The investment in this plan do not have any vesting age – one can start investing soon after the birth of the child and one can withdraw money after the child reaches a certain age. Some child policies offer intermediate withdrawal options as well. This can be either a ULIP or an endowment plan.

Retirement or Annuity Plan

Retirement or Annuity PlanTaking insurance policies for the sake of the family is not enough. One should also keep one’s old age in mind. When you are young you have a regular source of income, but during old age the situation can change. So, one needs to plan for the retirement also. Along with coverage, retirement or annuity plans give the option of saving and investing money which can be used in the old age. Life insurance companies in India provide retirement plans which help create a corpus from which a regular income, called annuity or pension, is given to the insured after reaching a certain age.

Retirement plans can be availed “with cover” or “without cover”. The first plan offers a sum assured to the beneficiary and the “without cover” one gives the corpus amount to the beneficiary only after the death of the insured.

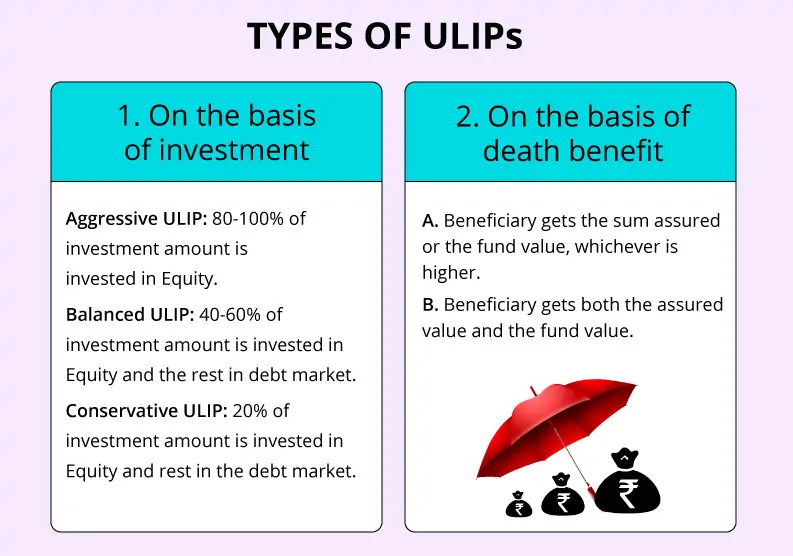

Unit Linked Insurance Plan (ULIP) offers dual advantage – coverage and a means of investment. Under this plan, the cash value/paid up value of the policy depends on the current asset value. The total premium paid by the insured is divided into two parts: one that is invested in the market or debt funds and the other that is used for insurance. The type of investment is selected by the insured depending on the type of risk that he/she is willing to take.

On basis of investment:

On basis of death benefit:

Group life insurance is a type of life insurance that covers a group of people. It is mostly provided by companies to its employees. As the insurance is done in a group, a group life insurance is considered cost-effective. The group can comprise lawyers, members of cooperative banks, societies, doctors, etc. This life insurance can be contributory, where the employees contribute along with the employer in the payment of the premium, or non-contributory, where the employer pays the entire premium amount.

You can brave various situations of life when you are young; however, in old age you need more protection and security. To manage such circumstances of life in old age, life insurance for senior citizens can be a good option. The insurance also provides financial coverage at times of need. For instance, in case you do not have any support for your spouse, life insurance for senior citizens can provide financial security to the spouse in case of your sudden demise. The death benefit can also be used to manage loans, debts and other financial needs.

Along with the standard coverage which varies with plan to plan, you can further enhance the protection with the help of riders, such as accidental death benefit rider, total or permanent disability rider and many more. The additional benefits can be availed on payment of some extra amount. Following are some common riders:

| Particulars | Details |

| Entry Age | 18-75 years |

| Policy Term | 5-75 years |

| Premium Payment Option | Regular, limited and single premium |

| Sum Assured | Rs 3 Lakh-100 Crore |

Following are the standard set of documents required to process a claim:

In case of untimely demise of the insured, the nominee or beneficiary can file a claim to get the sum assured.

A life insurance policy protects the insured and his family against different scenarios, but certain claims are not covered by the insurance company. Below are some common exclusions. However, this might vary for different policies.

After informing the insurance company about the death of the insured, the claimant needs to submit the required documents, along with the claim form. The insurance company takes something like a week to a month to evaluate and approve or reject the claim. Settlement of a claim usually takes one or two months and in case it takes more time than specified, the insurance company might pay late payment interest on the sum assured. However, insurance companies also take the initiative to keep the nominee posted about the status of the claim.

There are 24 insurance companies providing life insurance policies in India. They are listed here according to their Claim Settlement Ratio (CSR) for 2017-18. A CSR is the total claims paid compared to the total claims received in a financial year.

Since there are many companies selling insurance policies, selecting a particular company and a policy is a big task. To ease this process, you should keep certain points in mind.

Below are some common terms related to life insurance:

Maturity Age: Every life insurance policy comes with the maturity age at which the policy ends. Basically, Life Insurance Company will beforehand communicate to the insured about the maximum age till which the coverage will be provided to the insured.

Premium: It is the amount which the life insured pays to the company in exchange for policy and the sum assured.

Premium Payment Term: The duration of paying the premium. It can be regular (monthly, annually), limited payment term and single payment.

Nominee: It is the legal heir chosen by the policyholder to whom the sum assured will be paid after the demise of life insured by the insurance company. The nominee could be wife, child and parents of the policyholder.

Sum Assured: It is the amount that the insurance company agrees to pay on death of the insured person to the nominee.

Riders: They are additional features or extra protection you can get on the payment of some extra amount. Riders increase the base cover and protect the insured against unexpected circumstances.

One needs the following documents to buy a policy:

One can increase the protection with the help of additional riders, such as accidental death cover, critical illness, disability cover, on the payment of additional amount along with the premium. These riders will protect the insured against a host of unexpected situations.

In a term insurance plan, you usually do not get back the premiums paid, in case you happen to survive the policy. However, there are some plans that offer this survival benefit along with the death benefit. Some of the policies offering this benefit in India are Max Life Premium Return Protection Plan, Tata AIA Life Insurance iRaksha Trop and Aegon Life iReturn Insurance Plan.

No. Suicidal deaths do not qualify for claims by any insurance company.

Usually every insurance company provides a ‘free look period’ which lasts for 15-30 days. If you cancel within this period, you will be eligible for a refund (less certain charges). This period starts right after you have made the payment.

There is no single age which can be labelled as the best age for buying a life insurance plan. However, it is suggested to purchase a suitable life insurance plan at a younger age, usually before you hit 30-35 years. At such young age, the premiums are also comparatively lower.

Yes, with certain conditions, multiple policies can be opted for.

If you are a smoker, chances are you will be asked to pay comparatively higher premium as compared to your counterparts. This amount can be huge or meagre, depending on your age, gender and also on the company from which you are buying the insurance.

It is advisable to purchase a joint life insurance plan instead of separate ones as the premiums can be clubbed and chances are you may get discount on the same too.