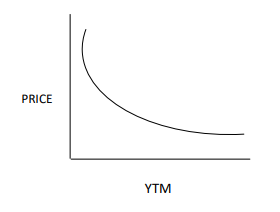

Bond convexity is a measure of the curvature in the relationship between the bond prices and bond yields. In other words, the degree of sensitivity of a bond to interest rate fluctuations - not just in a straight line, but along a curve. The term is a second-order derivative of the price equation and is relevant in the context of bond risk management strategy.

Bond ConvexityWhy MattersFormula & ExampleConvexity vs DurationPositive & Negative ConvexityBonds Having Higher ConvexityFAQs

Bond Convexity

Bond convexity is a crucial concept that helps investors to understand how bond prices respond to changing interest rates environments than the duration estimates. By understanding convexity, investors can compare bonds more effectively and understand risk management, especially in volatile market conditions.

High returns

Earn fixed returns of up to 13.25%

Low investment

Start investing with as little as ₹1,000

Low risk

Invest in AAA–BBB rated bonds

No brokerage

0% brokerage or commission fees

4.5/5

15.6L Reviews

5.7cr+Satisfied Customers

₹3,064 CrsInvestment Enabled

100+Bonds

Invest as Low as ₹1000 & Getup to 13.25% Returns

High returns

Earn fixed returns of up to 13.25%

Low investment

Start investing with as little as ₹1,000

Low risk

Invest in AAA–BBB rated bonds

No brokerage

0% brokerage or commission fees

4.5/5

15.6L Reviews

5.7cr+Satisfied Customers

₹3,064 CrsInvestment Enabled

100+Bonds

Explore Bonds by Category

High Yield

CARE BBB-

You Invest

₹9,989

Returns (YTM)

13.75%

You Get

₹12,457

Today

27 months

Profitable, Listed NBFC with 50+% Capitalisation

You Invest

₹9,989

Returns (YTM)

13.75%

You Get

₹12,457

Today

27 months

Profitable, Listed NBFC with 50+% Capitalisation

CARE BBB-

INFOMERICS BBB

You Invest

₹1,99,543

Returns (YTM)

13.75%

You Get

₹2,66,950

Today

36 months

Best Capital June'29

You Invest

₹1,99,543

Returns (YTM)

13.75%

You Get

₹2,66,950

Today

36 months

Best Capital June'29

INFOMERICS BBB

CARE BBB-

You Invest

₹10,006

Returns (YTM)

13.65%

You Get

₹12,669

Today

29 months

Profitable, Listed NBFC with 50+% Capitalisation

You Invest

₹10,006

Returns (YTM)

13.65%

You Get

₹12,669

Today

29 months

Profitable, Listed NBFC with 50+% Capitalisation

CARE BBB-

What is Bond Convexity

How to Buy Bonds through Paisabazaar?

Get up to 13.25% from bonds in 5 simple steps

Step 1: Login to your Paisabazaar account

Step 2: Select the Bonds

Step 3: Complete the KYC process

Step 4: Enter bank details

Step 5: Link your demat account

Understanding Why Bond Convexity Matters

To understand the concept of bond convexity, we need to understand the ‘duration’, which is considered the first order derivative of the bond price equation. Duration measures how sensitive your bond is to changes in interest rates. It assumes a linear relationship between bond yield changes and changes in price. But, this relationship isn't actually linear when interest rates change by large shifts—it's curved. Convexity corrects this error and provides a more accurate prediction.

Example

To understand convexity and duration better, let me compare it to driving a car. The speed of the car is referred to as the duration. While the driver is speeding up or slowing down (i.e., the rate of change), the car is called convexity. In relation to the bond market, the higher the convexity, the more drastic the change would be in the price given a move in interest rates.

Formula for Calculating Bond Convexity

Convexity = (1 / P) * Σ [(Ct * (t² + t)) / (1 + y)^(t+2)]

Where:

‘P’ is the current price of the bond

‘Ct’ is the cash flow at time ‘t’

‘y’ is the yield to maturity

‘t’ is the time period in years

Let's take an example

ABC Ltd. has issued bonds having a face value of Rs 1,000 with a coupon rate @ 10% p.a. The maturity period of the bond is 3 years. The yield to maturity is 10% and the prevailing current bond price is Rs 1,000.

Let’s calculate convexity:-

First, we need to identify cash flows, i.e., ‘Ct’

| Year | Cash Flow |

|---|---|

| 1 | 100 |

| 2 | 100 |

| 3 | 1,100 (1,000 +100) |

Now, applying the bond convexity formula:-

For the year 1

Cash Flow (Ct): 100

Time period (t): 1

Yield to maturity (y) = 10% = 0.10

Convexity: [(100 * (1² + 1)) / (1 + 0.10)^(1+2)] = 150.26

For the year 2

Cash Flow (Ct): 100

Time period (t): 2

Yield to maturity (y) = 10% = 0.10

Convexity: [(100 * (2² + 2)) / (1 + 0.10)^(2+2)] = 409.77

For the year 3

Cash Flow (Ct): 1100

Time period (t): 3

Yield to maturity (y) = 10% = 0.10

Convexity: [(1100 * (3² + 3)) / (1 + 0.10)^(3+2)] = 8197.45

Summing the values of convexity

150.26+ 409.77+8197.45 = 8757.48

Dividing by bond’s price = 8757.48/1000 = 8.757 or 8.76

The value 8.76 means the bond has positive convexity.

People also search for

Difference between Convexity & Duration

| Differentiation Factor | Convexity | Duration |

|---|---|---|

| Relationship | Measures the curvature of the price-yield relationship | Assumes linear relationship - straight line |

| Measures | Change in price sensitivity | Price sensitivity |

| Calculus Order | Second derivative of price-yield function | First derivative of price-yield function |

| Accuracy Level | Accurate for large interest rate movements | Accurate for small interest rate changes |

| Impact When Interest Rates Fall | Predicts higher price appreciation than the duration predicts | Predicts price increase using a straight-line estimate |

| Impact When Interest Rates Rise | Shows a smaller price decline than the duration predicts | Predicts price decline using a linear estimate |

Suggested Read : Government Bonds vs Corporate Bonds

Positive Convexity & Negative Convexity

Positive convexity refers to a bond's price rising faster when bond yields fall and falls slower when yields rise. This benefits investors with more upside than downside, which is seen in most regular corporate bonds, government bonds, or plain vanilla bonds. Negative convexity is seen in callable bonds, as such bonds have a ceiling on their price. When interest rates fall, bonds are usually called, i.e., limiting upside for investors. And, when interest rates rise, the bond won't be called, i.e., full downside for investors. This creates a negative convexity, which hurts investors by limiting upside and worsening losses.

Bonds Having Higher Convexity

Zero-coupon bonds, non-callable corporate bonds and long-term government bonds have higher convexity. Zero coupon bonds have higher convexity because their entire cash flow is received at the maturity period. This makes the present value of the bond extremely sensitive to interest rate changes in the market, which results in a pronounced curve in the price-yield relationship. The price swings are high for bonds with longer maturity periods.

Is Higher Bond Convexity Good?

Higher positive convexity is considered good for investors because it offers greater upside potential and downside protection. Upside potential here refers to the faster increase in the bond's price when interest rates fall and downside protection means the bond's price falls less when interest rates rise. However, such bonds often come with lower yields and higher prices. Therefore, investors should balance high bond convexity benefits with their investment objectives and the return potential. Ignoring convexity in the portfolio can lead to underestimating the bond risk during an environment of sharp rate movements.

How to Buy Bonds through Paisabazaar?

Get up to 13.25% from bonds in 5 simple steps

Step 1: Login to your Paisabazaar account

Step 2: Select the Bonds

Step 3: Complete the KYC process

Step 4: Enter bank details

Step 5: Link your demat account

FAQs

Is bond convexity good or bad?

Bond convexity (positive) is good for investors. It means a bond's price rises faster when interest rates fall and loses less when rates rise. This improves return potential and better risk management from interest rate movements. However, not all bonds have positive convexity, such as callable bonds.

What causes negative convexity?

Negative convexity is seen in Mortgage-backed securities (MBS) and callable bonds, as such bonds have a ceiling on their price. In callable bonds, when interest rates fall, bond is usually called because issuers are more likely to refinance debt at a lower cost. This limits upside for investors. And, when interest rates rise, the bond won't be called, i.e., full downside for investors. This creates a negative convexity.

Can a bond have zero convexity?

Short term bonds can have a zero convexity or near to zero convexity. Callable bonds or mortgage-backed securities have negative convexity due to a ceiling in price.

Why should I care about convexity if I’m holding to maturity?

Convexity still matters even if you hold bonds till maturity, as it measures how much your bond's price actually changes with large rate swings. This offers better risk management and portfolio volatility. It also helps investors to manage interest rate risk during periods of sharp interest rate movements.

Is higher bond convexity better?

Higher positive convexity is better, as it leads to faster price appreciation when interest rates fall and slower price declines when interest rates rise. This provides cushion to bond investors against market volatility and better returns in changing interest rate environments, though the bonds may come with lower yields.

Which bonds have the highest convexity?

Bonds in India with the highest convexity include zero coupon bonds, due to longer effective duration, long-term government bonds and corporate bonds without embedded options. Long duration bonds respond sharply to interest rate changes, making them suitable for investors seeking portfolio diversification and stronger interest rate sensitivity.

Bonds Articles

How to Choose Between Fixed & Floating Rate Bonds

Bhumika Khandelwal20 May 2026

How to Check Bond Credit Rating

Bhumika Khandelwal13 May 2026

How to Buy Corporate Bonds Online

Bhumika Khandelwal21 Apr 2026

NRI Bonds for USA: How NRIs Living in the US Can Invest in Indian Bonds

Sourabh Kumar14 Apr 2026

How NRIs Can Invest in Corporate Bonds

Paisabazaar31 Mar 2026

Digital Gold vs SGB

Bhumika Khandelwal10 Mar 2026

Bonds vs Mutual Funds – Which Investment Option is Right for You?

Paisabazaar25 Feb 2026

Sovereign Gold Bond vs Gold ETF – Which is Better?

Bhumika Khandelwal24 Feb 2026

Convertible Bond vs Non-Convertible Bonds

Bhumika Khandelwal13 Feb 2026

How to Invest in Government Bonds

Vandana Punj12 Feb 2026

Written By

Bhumika KhandelwalReviewed By

Shamik GhoshCheck Top Bond Offers with Assured Returns of up to 13.25%

Paisabazaar is a loan aggregator and is authorized to provide services on behalf of its partners

*Applicable for selected customers