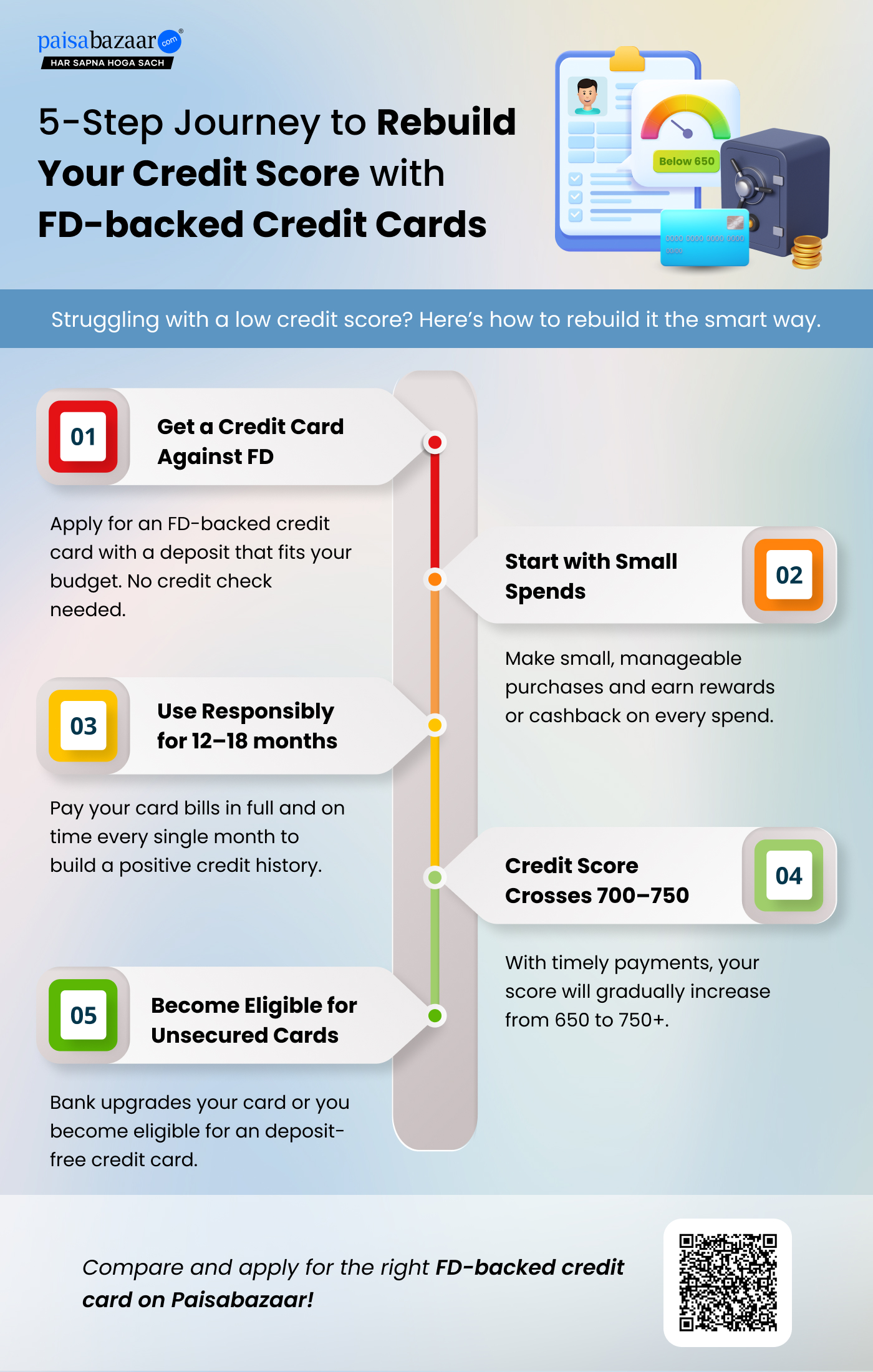

A missed EMI, delayed payment, or no credit history at all can lead to credit card declines, loan rejections, and limited financial options. However, you can rebuild your credit score with an FD-backed credit card, even without income proof or a strong credit history.

FD-backed credit cards are one of the easiest and most effective ways to improve your credit score and become eligible for unsecured credit cards in the future. Since the fixed deposit acts as collateral, banks are more willing to issue these cards even if your credit score is low or damaged. With responsible usage and financial discipline, you can gradually rebuild your credit profile. Read on to understand how FD-backed credit cards can help you improve your credit score.

What is an FD-backed Credit Card?

An FD-backed credit card, also known as a secured credit card, is a credit card issued against a Fixed Deposit (FD) that you place with the bank as collateral.

Here's how it works:

1. You open a Fixed Deposit, typically starting from Rs. 2,000, depending on the bank

2. The bank issues credit card with a credit limit that is usually 80–90% of your FD amount

3. You use the card for everyday transactions and pay your bills on time

4. Your repayment behaviour is reported to credit bureaus (CIBIL, Experian, CRIF), and your credit score starts improving

How FD-backed Credit Cards Can Rebuild Your Credit Score

When you use an FD-backed credit card and pay your dues on time every single month, here's what happens to your credit profile:

On-time Payment History Builds Up

Payment history is one of the most important factors in determining your credit score. When you use an FD-backed credit card and consistently pay your bills on time, it creates a positive repayment track record. Even a few months of timely payments can start improving your creditworthiness. Over time, this positive payment history signals to lenders that you are a reliable borrower, making it easier for you to get approvals unsecured credit cards in the future.

Activity Reported to Credit Bureaus

FD-backed credit cards function just like regular credit cards when it comes to credit reporting. Banks report your usage, repayments, and outstanding balances to credit bureaus like CIBIL, Experian, and Equifax. This means every action, such as timely payments, low credit utilization and more, gets reported to credit bureaus, which can help you build a positive credit profile.

You Credit Score Starts Improving

As you continue using your FD-backed credit card responsibly, your credit score gradually starts improving. Factors like timely payments, low credit utilization, and consistent usage all contribute positively to your score. While the improvement may not be instant, you can typically start noticing changes within 12-18 months. Over time, this steady progress can help you move from a low or no credit score to a strong credit score, preferable above 750, making you eligible for unsecured credit cards with better benefits.

Your Credit Age Grows

Credit age refers to how long you have been using credit. The longer your credit history, the better it is for your credit score. In addition to the above factors, starting early with an FD-backed credit card and keeping it active over time, you increase your overall credit age. A longer credit history with positive repayment behaviour, improves your credit profile and increases your chances of getting approved for unsecured credit cards in the future.