Download the

Paisabazaar app Today!

Paisabazaar app Today!

Get instant access to loans, credit cards, and financial tools — all in one place

Win Assured Cashback

Our Advisors are available 7 days a week, 9:30 am - 6:30 pm to assist you with the best offers or help resolve any queries.

Get instant access to loans, credit cards, and financial tools — all in one place

Scan to download on

Our Advisors are available 7 days a week, 9:30 am - 6:30 pm to assist you with the best offers or help resolve any queries.

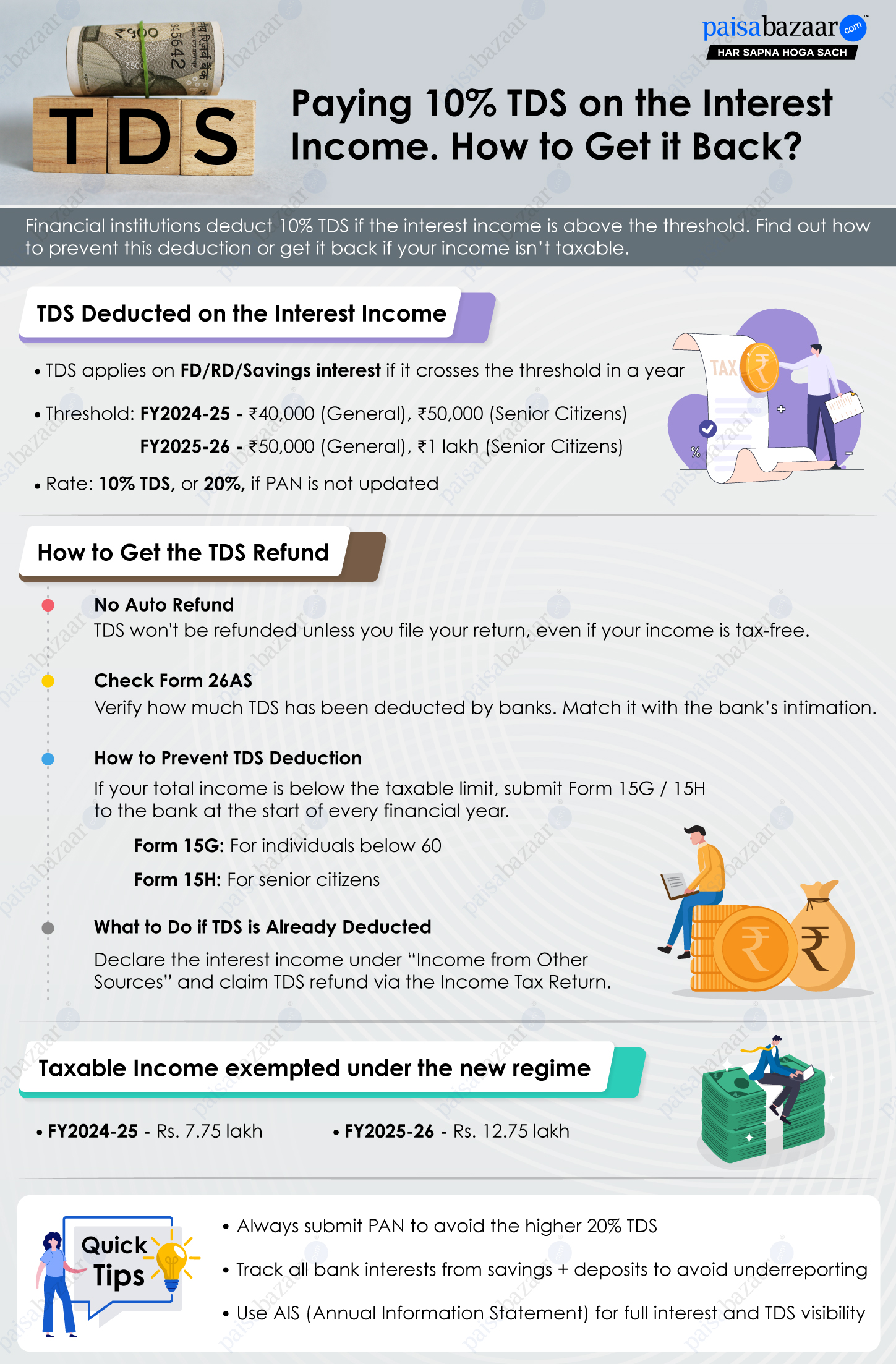

A certain amount of interest income is exempt from income tax for all taxpayers. The bank adds up the interest amount from all your accounts across its branches to check if it crosses the exemption limit.

When this exemption limit is crossed, the financial institution deducts tax against your PAN and deposits it with the Income Tax Department. Even when you don’t fall under the taxable income slab, you end up paying the tax through TDS. Let us understand how to get this amount back or prevent this amount from being deducted.

TDS or Tax Deducted at Source is the amount deducted by the payer (bank) at the time of making the payment to the payee (beneficiary). The TDS deducted is mentioned in Form 26AS and is deposited with the Income Tax Department against your PAN.

Suggested Read: Know Everything about PAN Card

Banks and financial institutions deduct TDS on the interest income through various financial instruments such as savings accounts, fixed deposits, SCSS, POMIS, etc., when the interest income exceeds a certain limit. The exemption limit is mentioned below:

| Investment Year | Exemption Limit | |

| General Citizens | Senior Citizens | |

| FY 2024-25 | Rs. 40,000 | Rs. 50,000 |

| FY 2025-26 | Rs. 50,000 | Rs. 1 lakh |

If the interest earned by you through various savings schemes is above this exemption limit, TDS at a rate of 10% is deducted by the bank.

In case you do not furnish your PAN against these investments, TDS at a rate of 20% is deducted by the bank. It is worth noting that for any financial transaction above Rs. 2 lakh, you have to furnish your PAN, without which your transaction would not be realised.

Also Read: Savings Account Interest Rates

It is worth noting that you become eligible to pay taxes only if your total income exceeds the exemption limit. The maximum possible exemption limit is mentioned in the table below:

| Financial Year | Old Regime (in Rs.) | New Regime (in Rs.) |

| 2024-25 | 5.5 lakh | 7.75 lakh |

| 2025-26 | 5.5 lakh | 12.75 lakh |

Note: The exemption limit is inclusive of the allowed standard deduction.

In case your taxable income after all deductions is up to Rs. 5.5 lakh, you can choose the old regime. However, if your taxable income is up to Rs. 7.75 lakh, you can choose the new regime for FY2024-25. It is noteworthy that no deductions are allowed under the new tax regime.

The good news is that this exemption limit has been increased to Rs. 12.75 lakh starting FY 2025-26. However, no such increment has been proposed in case of the old tax regime for FY 2025-26 and the existing Rs. 5.5 lakh with deductions still prevails.

If you don’t fall in the taxable income bracket and you don’t want the bank to deduct TDS on the interest earned, you can submit Form 15 and request the bank not to deduct any TDS.

Regular citizens need to submit Form 15G, and senior citizens are required to submit Form 15H at the start of every financial year to inform the bank that they do not fall under the taxable bracket.

When you fail to submit Form 15 G/H at the start of the year, the bank deducts the TDS on the interest amount. There is still a possibility of getting the refund of the deducted TDS.

You have to file the Income Tax Return every year by July 31st. When you file ITR, you have to mention the total income from all sources.

If your total income under the new regime is below Rs. 7.75 lakh for FY2024-25 and below Rs. 12.75 lakh for FY 2025-26, you are not liable to pay income tax. Any TDS deducted by a bank or financial institution can be claimed through this ITR.

Also Read: How to File ITR?

File your ITR diligently and validate the return request through eSign using Aadhaar OTP. The Income Tax Department shall scrutinise your application and issue a refund to the bank account mentioned in the ITR. This refund shall contain all TDS deductions carried out by the bank throughout the year.

Many taxpayers have faced an issue in the past, where the bank wasn’t able to share the ITR refund communication with the beneficiaries. So it is recommended to check your bank statement at the end of the month to see if the refund was issued. You can also check the refund status by logging into your Income Tax e-filing account.